Anthropic: From a $550 Million Startup to a $1 Trillion Phenomenon

In early 2021, Dario Amodei walked out of OpenAI with seven colleagues and $124 million in seed funding, valuing the new company at $550 million. Five years later, buyers in the private secondary market are bidding Anthropic shares at prices implying a valuation near $1 trillion — a roughly 1,800-fold increase in less than five years. This is not primarily a story about artificial intelligence. It is a story about how capital prices the future.

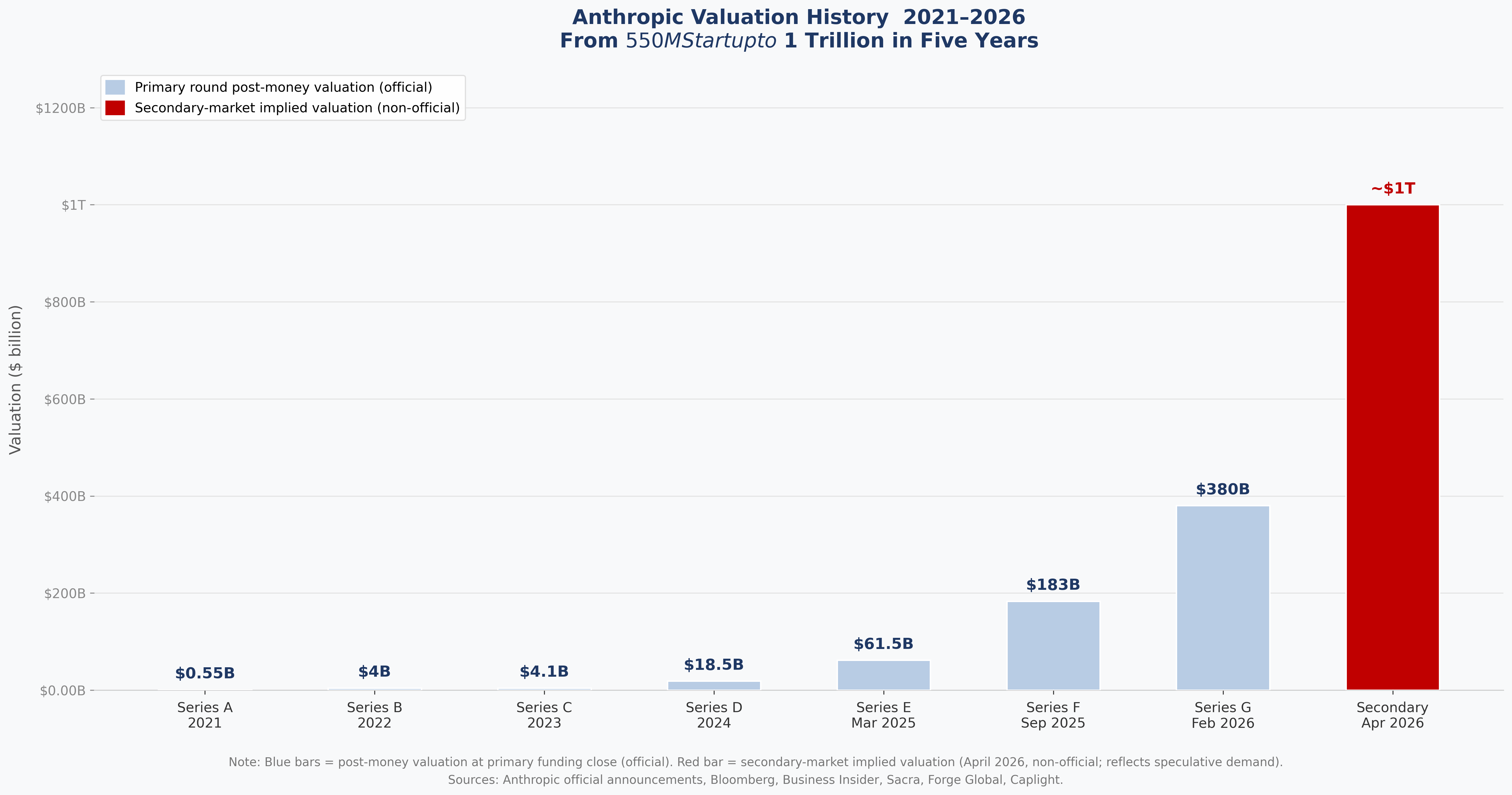

The chart below plots Anthropic’s post-money valuation at each primary funding round alongside the current secondary-market implied figure (red bar). That final bar is not an official fundraising valuation. It reflects the price at which existing shareholders — employees, early backers, VC funds — are selling shares to new buyers on private-market trading platforms. It carries a speculative premium. It is, however, the most current coordinate the market has assigned to Anthropic.

1. The $1 Trillion Signal: What Secondary Markets Are Saying

On April 23, 2026, Business Insider reported that Anthropic’s implied valuation on private secondary-market platforms had reached approximately $1 trillion. That figure is more than 2.6 times the $380 billion post-money valuation Anthropic achieved in its Series G round just ten weeks earlier, and it surpasses OpenAI’s roughly $880 billion secondary-market price on the same platforms. Among privately held companies globally, only SpaceX commands a higher implied valuation. Anthropic ranks second.

1.1 Primary rounds vs. secondary markets: why the distinction matters

When a company closes a primary funding round, new investors wire money directly into the company’s bank account. Both sides negotiate a valuation; the resulting figure is legally binding and endorsed by all shareholders. Secondary-market transactions are different: existing holders — employees sitting on vested options, early-stage VCs, angel investors — sell their shares to new buyers. The company receives nothing and is not a party to the deal. The implied valuation is reverse-engineered from whatever price buyer and seller agree on.

The bottom line: Anthropic has not raised money at a $1 trillion valuation. The company has declined to comment on secondary-market pricing.

1.2 Where the numbers come from

Business Insider cited multiple independent sources active in private-share markets:

• Forge Global CEO Kelly Rodriques told Business Insider the implied valuation was “hovering around the $1 trillion mark.”

• Glen Anderson of Rainmaker Securities said he had just been offered shares at an implied value of $960 billion — a figure he called “unthinkable” just a month earlier — and that those shares were snapped up by competing buyers within hours.

• Ken Sawyer, co-founder of Saints Capital, noted that one Anthropic shareholder was willing to sell at an implied valuation of $1.15 trillion.

• A “very prominent growth fund” offered AI startup founder Jesse Leimgruber — an Anthropic secondary-market shareholder — $1.05 trillion for his shares.

1.3 Why the price jumped from $800 billion to $1 trillion in two weeks

Around April 14, Bloomberg and Business Insider reported that venture capital firms had approached Anthropic with preemptive-round offers valuing it at $800 billion or more. At that point, Caplight — a platform that tracks private-share transactions — was recording an implied valuation of roughly $688 billion, up about 75% from the Series G close. In the two weeks that followed, prices jumped further toward $1 trillion. Two structural forces drove the move:

Revenue is accelerating faster than anyone expected. Anthropic’s annualized revenue run rate stood at roughly $9 billion at the end of 2025. By March 2026, it had reached $30 billion — a 233% increase in a single quarter, driven primarily by enterprise adoption of Claude Code and broader API usage.

Anthropic has turned down new primary-round offers. Bloomberg reported that Anthropic has declined overtures from VCs seeking to lead a new primary round. With no fresh primary shares available, every dollar of demand flows into the secondary market, where supply is scarce and competition among buyers is driving prices higher. Reports emerged of buyers pledging real estate as collateral to fund Anthropic share purchases.

1.4 OpenAI is moving in the opposite direction

On the same platform where Anthropic commands a near-trillion implied valuation, OpenAI trades at roughly $880 billion — only 3% above the $852 billion post-money valuation from its early-2026 primary round. Caplight data showed a five-to-one ratio of sellers to buyers in OpenAI shares in Q1 2026, a sharp reversal from late 2025, when buyers dominated. Glen Anderson described OpenAI demand as “tepid,” with some bids coming in below the company’s last primary valuation. The two most-watched AI companies are telling radically different stories in the private market right now.

Important caveat: secondary-market prices do not mean Anthropic could raise primary capital at $1 trillion, nor that an IPO would price there. These are prices paid for illiquid minority stakes with no board rights and no guarantee of liquidity. They reflect speculative demand as much as fundamental value. At $1 trillion, Anthropic trades at roughly 33 times annualized revenue — rich by any historical standard, though not unprecedented for a company growing this fast.

2. Google’s $40 Billion Bet on Its Own Rival

On April 24, 2026, Alphabet’s Google announced an investment of up to $40 billion in Anthropic — the largest single strategic capital move in the two months since the Series G closed. The investment is not a new funding round; it is a strategic extension of the Series G, executed at the same $350 billion pre-money valuation.

The deal has two tranches, per Anthropic’s official announcement and Bloomberg reporting: $10 billion in immediate cash, wired upon signing; and up to $30 billion tied to specific Anthropic performance milestones. Alongside the equity investment, Google Cloud committed to supply 5 gigawatts of TPU compute capacity over five years, with the option to expand further — among the largest single-supplier compute commitments ever made to an AI company.

The logic behind Google investing billions in a direct competitor is straightforward: Anthropic is one of Google Cloud’s most important enterprise customers. The TPU purchases at scale drive Google Cloud revenue directly. Before this deal, Google had invested roughly $3 billion in Anthropic across multiple tranches since 2023, accumulating approximately 14% equity. Adding the new $10 billion immediate and up to $30 billion conditional brings Google’s total capital commitment to approximately $43 billion — one of the largest strategic investments any company has ever made in a direct competitor.

“Shareholder and infrastructure supplier simultaneously — Google’s relationship with Anthropic is the defining case study in AI-era coopetition.”

3. Amazon’s $5 Billion Investment and a $100 Billion Cloud Pledge

Four days before Google’s announcement, on April 20, Amazon injected a fresh $5 billion in cash into Anthropic and reserved an additional $20 billion tied to commercial milestones. In exchange, Anthropic committed to spend more than $100 billion on AWS over the next ten years and secured access to up to 5 gigawatts of Trainium and Graviton compute — with additional Trainium2 capacity (separate from the Project Rainier cluster already operational since October 2025) coming online in the first half of 2026, and nearly 1 GW of combined Trainium2 and Trainium3 capacity expected by year-end.

The April investment brought Amazon’s cumulative cash in Anthropic to $13 billion, making it the single largest institutional investor in the company. If the full $20 billion conditional tranche triggers, Amazon’s total commitment would reach $33 billion. Bloomberg noted that Amazon negotiated the same $350 billion pre-money valuation as Google — a structural advantage that comes from being both an investor and the company’s primary infrastructure provider.

These two deals crystallize the defining logic of large-cap AI investment in 2026: deploy X billion in equity capital, secure X-times-X in cloud-spending commitments, and hold a front-row seat for the IPO upside. The boundary between “investment” and “anchor customer contract” has effectively ceased to exist.

4. The Valuation Arc: From $350 Billion to a $1 Trillion Bid

To place the April strategic investments in context, consider where they sit relative to the Series G, which closed on February 12, 2026. The round raised $30 billion at a $350 billion pre-money / $380 billion post-money valuation, led by Singapore’s sovereign wealth fund GIC and Coatue, with D.E. Shaw Ventures, Dragoneer, Founders Fund, ICONIQ, and MGX co-leading, alongside previously announced strategic commitments from Microsoft and Nvidia. At the time of closing, the Series G was the second-largest private funding round in history.

Both the Amazon and Google investments were executed at the same $350 billion pre-money figure, meaning they are effectively strategic extensions of the Series G rather than a new valuation anchor. As the two tranches of immediate cash — totaling more than $15 billion — land on Anthropic’s balance sheet, the actual capital raised since February now substantially exceeds what the $380 billion post-money figure implied at closing.

The sharpest signal of where the market now sits comes from secondary trading. As detailed in Section 1, Caplight tracked an implied valuation of roughly $688 billion in mid-April, with Forge Global reporting near-$1-trillion bids by April 23. Anthropic has not accepted any of the VCs’ preemptive primary-round offers and declined to comment.

“Bloomberg and Business Insider reported: VCs have bid $800 billion-plus; Forge Global shows secondary buyers approaching $1 trillion. Anthropic has said no to a new primary round — for now.” (TechCrunch, April 15, 2026)

5. The Full Funding Journey: $550 Million to $1 Trillion in Five Years

Anthropic was founded in January 2021 by Dario Amodei, Daniela Amodei, and several former OpenAI researchers under the banner of “safety-first AI.” It has since completed one of the most concentrated capital accumulation paths in the history of private markets.

5.1 2021–2022: True believers and controversial capital

The company raised a $124 million Series A in the year of its founding at a $550 million valuation, led by Facebook co-founder Dustin Moscovitz and Skype co-founder Jaan Tallinn. In April 2022, a $580 million Series B came in led by FTX founder Sam Bankman-Fried — Alameda Research alone contributed $500 million for roughly 8% of the company. The FTX collapse later cast a shadow over this round, though Anthropic had already deployed the capital and emerged unscathed. Valuation: approximately $4 billion.

5.2 2023: The hyperscalers arrive

Claude 1 and 2 launched publicly. Enterprise adoption became measurable. Google invested approximately $300 million in February 2023 for roughly 10% equity, then followed with an additional $1.7 billion later that year. Amazon announced a phased commitment of up to $4 billion (the first $1.25 billion arrived in 2023), naming AWS as Anthropic’s primary cloud provider. In May 2023, Spark Capital led a $450 million Series C at a valuation of approximately $4.1 billion.

5.3 2024: Building the financial foundation

In February 2024, Menlo Ventures led a $750 million Series D valuing Anthropic at roughly $18.5 billion. Amazon’s remaining $2.75 billion arrived in March; a further $4 billion followed in November, bringing Amazon’s total to $8 billion. Claude 3 (Opus, Sonnet, Haiku) launched in March and for the first time traded benchmarks blow-for-blow with GPT-4.

5.4 2025: The megafunding era begins

In March 2025, Lightspeed led a $3.5 billion Series E at a $61.5 billion post-money valuation. Google co-invested $1 billion, reaching approximately 14% ownership. Six months later, in September 2025, ICONIQ led a $13 billion Series F — co-led by Fidelity Management & Research and Lightspeed — at a $183 billion post-money valuation, tripling the valuation in half a year. Claude Code emerged as a breakout product, with annualized revenue surpassing $500 million by the September 2025 Series F close. Eight of the Fortune 10 became paying customers.

5.5 February 2026: Series G — the second-largest private round in history

$30 billion raised. $380 billion post-money valuation. GIC and Coatue leading. By this point, Crunchbase tracked Anthropic’s cumulative fundraising at nearly $67 billion. Adding the April Amazon and Google immediate cash tranches, trackable capital raised surpasses the $80 billion mark.

6. The Revenue Engine: $30 Billion ARR and Where It Comes From

The fundamental engine behind every valuation discussed in this article is Anthropic’s revenue trajectory. Bloomberg and Business Insider reported in mid-April 2026 that annualized revenue had topped $30 billion — up from roughly $1 billion at the end of 2024, $9 billion at the end of 2025, and $14 billion at the Series G close in February 2026. Sacra estimates the year-over-year growth rate at approximately 1,400%. Axios called it “the fastest revenue growth in American corporate history.”

Revenue is overwhelmingly enterprise-driven: roughly 80% comes from enterprise API usage. As of April 7, 2026, the company had more than 1,000 customers each spending over $1 million annually — double the 500-plus figure reported at the Series G close in February, with growth accelerating. Eight of the Fortune 10 are paying customers. Claude Code alone generates $2.5 billion in annualized revenue as of the February 2026 Series G close — up more than fourfold from $500 million at the Series F — and commands a 54% share of the AI coding-tool market, ahead of GitHub Copilot and Cursor. In the enterprise LLM API market broadly, Anthropic holds a 32% share, compared to OpenAI’s 25%.

One important accounting note: Anthropic reports cloud-reseller revenue on a gross basis — counting total end-customer spend on AWS and Google Cloud as revenue, with platform fees booked as cost. This inflates the headline number relative to net-reporting peers. Even under a net-revenue lens, the growth rate remains extraordinary. At $30 billion ARR against a near-$1-trillion implied valuation, the implied price-to-sales multiple is roughly 33 times — aggressive, but not without precedent for a company at this growth rate.

7. Compute: The Real Currency of the AI Arms Race

In the AI industry, “fundraising” and “compute contracts” have become functionally indistinguishable. Anthropic’s capital strategy makes this concrete. The Series G’s $30 billion was offensive financing. Amazon’s $100 billion cloud commitment and Google’s 5 GW TPU pledge are defensive compute lockups. Training a single frontier model now costs hundreds of millions to billions of dollars; access to compute, more than capital per se, determines a company’s position at the frontier. Anthropic is expected to spend roughly $19 billion on training and inference in 2026 alone — roughly equivalent to its current revenue run rate.

7.1 Project Rainier: the world’s largest AI cluster

The centerpiece of Anthropic’s AWS relationship is Project Rainier — named after the 14,410-foot stratovolcano visible from Seattle on a clear day. The cluster went live in October 2025, initially deploying nearly 500,000 Trainium2 chips across 30 data-center buildings in St. Joseph County, Indiana (each roughly 200,000 square feet), plus additional sites in multiple U.S. states. According to AWS Distinguished Engineer Ron Diamant, Project Rainier is “the most ambitious undertaking AWS has ever attempted” — 70% larger than any prior AWS AI infrastructure deployment, and delivering more than five times the compute Anthropic used to train its previous generation of models.

Architecturally, the cluster uses a novel UltraServer design: four physical servers with 16 Trainium2 chips each, connected by dedicated NeuronLink high-speed interconnects that eliminate the latency of routing data through external network switches. Multiple UltraServers link into UltraClusters via Elastic Fabric Adapter networking, spanning buildings and data centers. AWS CEO Andy Jassy confirmed Anthropic was already running roughly 500,000 chips in Indiana and “doubled down on that order.” The cluster is on track to scale to more than one million Trainium2 chips by the end of 2026.

The next-generation chip, Trainium3, was developed in close collaboration with Anthropic, which provided direct design input on training throughput, latency, and energy efficiency. The new ten-year, $100 billion AWS commitment covers Trainium2 through Trainium4, with options on future generations.

7.2 Google Cloud: TPU scale-up and the Broadcom custom-chip deal

On April 6, 2026, Anthropic signed a new agreement with Google and Broadcom locking in 3.5 gigawatts of next-generation TPU capacity, expected to come online starting in 2027. This is one of the largest single custom-chip procurement announcements on record. Combined with the 5 GW TPU commitment attached to the April 24 investment deal and a prior commitment to access up to one million Google TPUs, Anthropic’s Google Cloud footprint now spans multiple generations of custom silicon.

7.3 CoreWeave: Nvidia GPUs and multi-cloud redundancy

On April 10, 2026, CoreWeave (Nasdaq: CRWV) announced a multi-year agreement to supply Anthropic with Nvidia GPU capacity across U.S. data centers, with compute coming online in the second half of 2026. CoreWeave now serves nine of the ten largest AI model providers; its shares jumped roughly 10% on the Anthropic announcement. The deal reflects Anthropic’s deliberate multi-architecture strategy: AWS supplies custom Trainium silicon, Google Cloud provides TPUs, CoreWeave provides Nvidia GPUs — ensuring that no single supplier can create a bottleneck.

The contrast with OpenAI’s infrastructure approach is instructive. OpenAI’s Stargate project is a concentrated $500 billion single-consortium cluster — a joint venture with SoftBank, Oracle, and MGX targeting 10 GW by 2029. Anthropic has built a distributed, multi-cloud hedge instead. Both strategies reflect the same underlying reality: frontier AI development now requires infrastructure at a scale previously available only to the world’s largest hyperscalers.

7.4 Fluidstack and the push toward owned infrastructure

In November 2025, Anthropic signed a $50 billion data-center partnership with UK-based neocloud provider Fluidstack, building facilities in Texas and New York that will come online throughout 2026 — Anthropic’s first major self-build infrastructure effort. On the same day as the CoreWeave announcement (April 10), Anthropic confirmed it is exploring the design of its own custom AI chips — following the paths already taken by Amazon (Trainium), Google (TPU), and Meta (MTIA). No dedicated chip team exists yet, but the direction is publicly confirmed.

The recent surge of user complaints about Claude rate limits is the product-side symptom of these compute constraints — and the reason Anthropic CFO Krishna Rao said the company needs to “keep pace with our unprecedented growth.”

8. The Investor Landscape: Who Holds the Equity, Who Captures the Upside

Anthropic’s cap table is dominated by strategic capital; pure financial VCs have relatively limited influence — a pattern now standard across frontier AI:

• Amazon ($13B cumulative, largest single investor): Primary cloud agreement, Project Rainier compute cluster. Amazon’s Q3 filing disclosed roughly $9.5 billion in pre-tax unrealized gains from the Anthropic stake.

• Google (~$3B historical + $10B immediate + up to $30B conditional): ~14% equity stake. Google’s Q3 filing disclosed approximately $10.7 billion in net income from an unnamed investment source, confirmed by persons familiar as Anthropic.

• GIC (Singapore sovereign wealth fund): Major investor in Series F; co-lead in Series G alongside Coatue. A flagship sovereign-capital bet on frontier AI infrastructure.

• ICONIQ Capital: Led Series F (alongside Fidelity and Lightspeed as co-leads); multi-round participant. Qatar Investment Authority co-invested at Series F.

• Lightspeed, Fidelity, Sequoia, Coatue: Core institutional VCs with positions across Series E, F, and G.

• Microsoft and Nvidia: Both announced up to $5 billion and $10 billion strategic commitments, respectively, in late 2025, with portions counted in the Series G.

9. “Safety First” as Competitive Advantage

In an industry where virtually every company claims to be “responsible,” does Anthropic’s Constitutional AI methodology and interpretability research constitute a genuine commercial differentiator? In enterprise procurement, the answer appears to be yes.

Anthropic’s enterprise customer base skews heavily toward compliance-sensitive sectors: financial services, legal, healthcare, and software development. Claude for Healthcare is a HIPAA-compliant offering with native integrations into the CMS Coverage Database and PubMed. In April 2026, Anthropic acquired biotech startup Coefficient Bio, extending its footprint into drug discovery and life-sciences research. The common thread across these verticals is that customers require AI that is predictable and auditable, not merely capable.

On the consumer side, Anthropic ran a Super Bowl ad in 2026 with the tagline “Claude will never run ads” — a direct shot at competitors testing ad monetization inside their AI products. The move extended the safety narrative from the research level to the mass-market level and reinforced Claude’s compliance image among enterprise buyers.

10. The IPO, the Spiral, and the Question Nobody Can Answer

At the current pace, an Anthropic IPO is less a question of whether than when and at what price.

10.1 Groundwork: lawyers, bankers, and a new board member

In December 2025, Anthropic retained Wilson Sonsini — the law firm that handled Google’s and LinkedIn’s IPOs — to begin the legal groundwork. Early in 2026, Chris Liddell joined the board. Liddell is the former CFO of Microsoft and the architect of GM’s $23 billion IPO; his appointment is one of the clearest signals Anthropic has sent about its public-market intentions. The company also completed a $5–6 billion employee tender offer in early 2026 at a $350 billion pre-money valuation, providing early employees with their first real liquidity window — standard operating procedure in the run-up to a listing.

The underwriting lineup is taking shape. Bloomberg reported that Goldman Sachs, JPMorgan, and Morgan Stanley are in early discussions for joint lead underwriter roles. The working timeline has an S-1 filing arriving in late summer 2026, a two-to-three-week roadshow in September, and a target listing window of October 2026 on Nasdaq. The offering is expected to raise more than $60 billion — which would make it the second-largest technology IPO in history, behind SpaceX if it lists first.

10.2 External pressure: Amazon’s conditions and the race with OpenAI

Two forces are accelerating the timeline beyond Anthropic’s own ambitions. First, Amazon’s investment agreement includes conditional tranches tied to Anthropic achieving specific IPO milestones — a contractual clock ticking in the background. Google’s ~14% stake will also achieve liquidity only through a public listing or an acquisition, providing further alignment between Anthropic’s two largest backers and a timely exit.

Second, OpenAI is targeting a late-2026 listing on a parallel track, and both companies are talking to the same small group of Wall Street banks. Whoever lists first captures the institutional allocation budgets. The competitive dynamic alone would push both companies toward the earliest workable window. Anthropic’s profitability roadmap also reads better in public markets: the company projects breakeven in 2028, while OpenAI is estimated to run $74 billion in operating losses that same year.

10.3 What public markets will demand

Public markets do not grade on a growth curve alone. Anthropic’s gross margin improved from -94% in 2024 to approximately 40% in 2025 — meaningful progress, but roughly 10 percentage points below its own targets, because inference costs ran 23% above projections. At the current burn rate, Anthropic will spend roughly $19 billion on training and inference in 2026, approximately matching its revenue. Net income will be deeply negative.

The gross-basis revenue accounting — booking full end-customer cloud spend as revenue — will draw scrutiny from sell-side analysts who will present net-basis comparisons. The IPO roadshow’s central challenge will be convincing institutional investors accustomed to SaaS valuation frameworks that a company spending nearly as much as it earns, at 33 times sales, deserves a premium multiple — and that the path to 2028 breakeven is credible.

10.4 The spiral — and the question worth asking

In early 2021, Dario Amodei’s team left OpenAI with $124 million, a $550 million valuation, and a plant-filled office in San Francisco. Five years later, the company has a $30 billion annualized revenue run rate, a secondary-market implied valuation near $1 trillion, and is preparing for one of the largest IPOs in the history of technology.

Beneath the numbers, a structural reality persists. Every massive fundraising round is simultaneously proof of commercial success and a pre-draw on future compute expenditure. More capital enables more aggressive training; more aggressive training compresses competitive advantage windows; compressed windows demand the next round of capital. It is a positive-feedback spiral with no obvious terminal point — different in kind from traditional technology scaling, where unit economics improve as scale increases. In frontier AI, the cost of staying at the frontier may scale non-linearly with capability.

An IPO is one of the few structural anchors in this spiral. It does not end the cash burn, but it changes who is asking the questions and on what timeline: from patient venture capital to quarterly earnings calls. Dario Amodei will need to explain to millions of public shareholders why a company with 40% gross margins, running near break-even, deserves a 33x revenue multiple — and why 2028 profitability is not merely a projection.

Perhaps the more important question is not whether Anthropic can go public, but whether the discipline of public-market accountability will change how faithfully it pursues the founding commitment that brought it into existence: safety first.

That question — more than any valuation figure — is the one worth watching.

Sources: Bloomberg, Business Insider (Forge Global, Rainmaker Securities, Saints Capital), TechCrunch, CNBC, Reuters, The Next Web, Crunchbase, Sacra, Anthropic official announcements, GIC press release, Amazon official announcement, CoreWeave official announcement, Data Center Knowledge, Data Centre Magazine, Wilson Sonsini client news, Augustus Wealth. Data as of April 25, 2026.