Buying OpenAI at a 70% Discount: How Thrive Capital Locked in $285B While Others Chase $800B

On February 25, 2026, CNBC cited sources familiar with the matter confirming that Joshua Kushner’s Thrive Capital invested approximately $1 billion into OpenAI around December 2025. At that time, the transaction gave OpenAI an implied valuation of approximately $285 billion, and the deal has already closed. CNBC also clarified that this was a secondary transaction—Thrive bought shares from existing shareholders rather than the company issuing new shares.

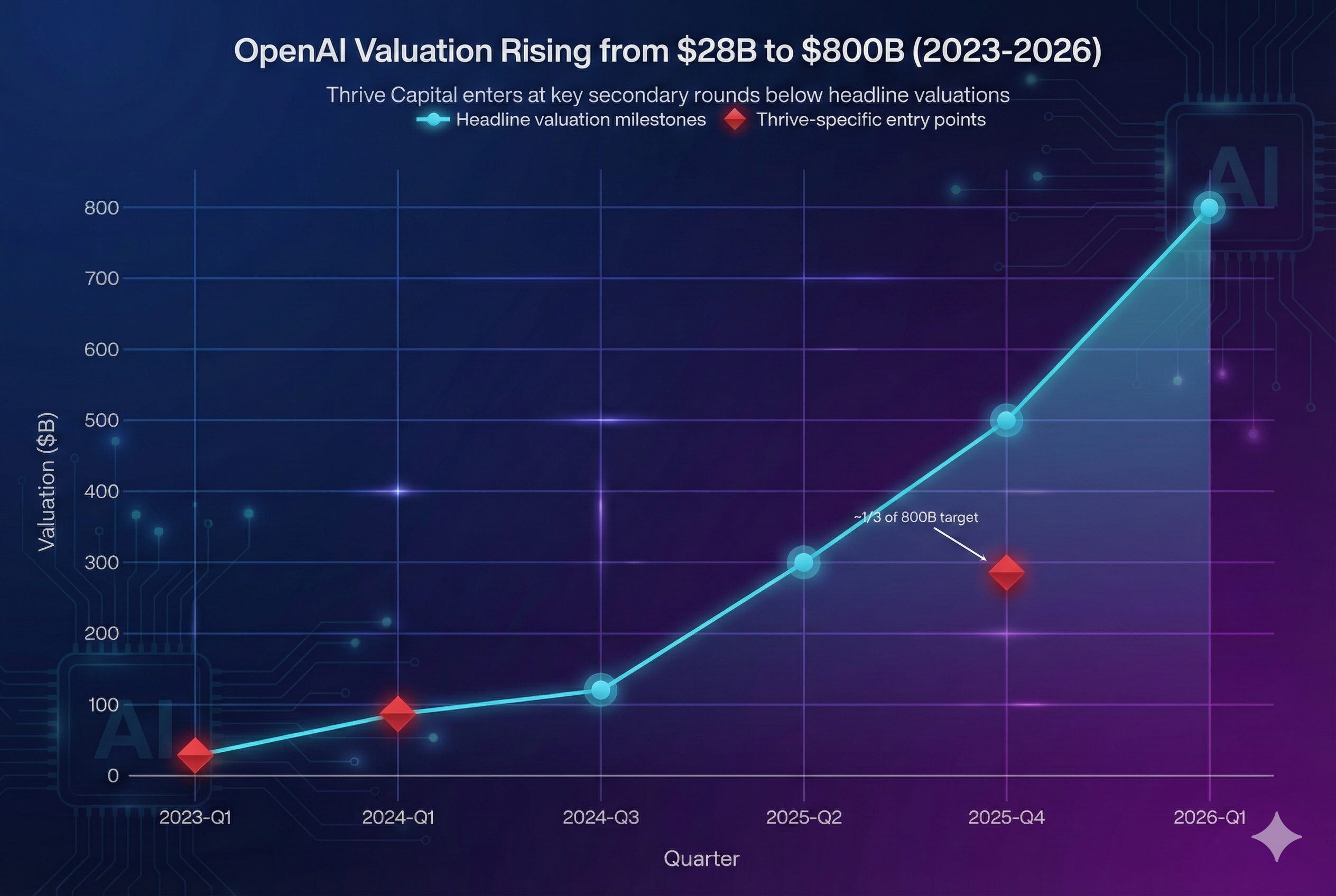

CNBC further pointed out that The Wall Street Journal was the first to disclose this investment. Subsequently, multiple media outlets provided comparative statements of an “approximate one-third discount” regarding the valuation and structure: $285 billion is about one-third of the over $800 billion target valuation OpenAI is currently pursuing.

At the same time, OpenAI is negotiating a new funding round with Middle Eastern sovereign wealth funds. Not only might the originally expected $50 billion minimum expand to a $100 billion scale, but its target valuation has also approached $830 billion or is even aiming for a trillion. This is a typical primary round: money enters the company to support the over $1 trillion in compute and infrastructure contracts that have already been signed upfront.

In other words—for the same company, within the same time window, there simultaneously exists a secondary transaction at a $285 billion valuation and primary negotiations targeting an over $800 billion valuation. This leads to the question you care about most: How exactly did Thrive manage to buy chips at a price that “looks like a 70% off discount”?

The following four sections will fully unpack the logic you want based on this factual foundation.

I. Starting with this “$285B Valuation” Entry: What Exactly is This Transaction?

The core points from reports like The Wall Street Journal are:

Transaction Scale and Valuation: Joshua Kushner’s Thrive Capital recently completed an OpenAI secondary transaction, buying shares from some existing shareholders/employees at an implied valuation of approximately $285 billion, which is roughly one-third of the current target valuation of over $800 billion.

Transaction Subject: This is not the company issuing new shares to Thrive (primary), but taking over shares from old shareholders/employees (secondary)—sellers prioritize liquidity and cashing out over maximizing valuation.

Timing: This $285B valuation transaction took place around December 2025, which was a block of shares locked in “before the $800 billion narrative was completely finalized.”

In other words: On the surface, it looks like a “one-third discount,” but in essence, it is “the price anchor of the previous stage’s secondary transaction being lifted by the sentiment of the subsequent primary financing.” It is not someone getting a “bone-deep special discount” in the same round.

II. The Complete Thrive–OpenAI Timeline: Snowballing from $27B to $800B

If you line up the publicly disclosed key milestones chronologically, you will see that Thrive’s position in OpenAI was built through “multiple rounds of stacked accumulation,” not just suddenly receiving preferential treatment today.

2023: First Time on Board — ~$27B–$29B Valuation

Multiple media outlets and analytical articles mention: Thrive’s first purchase of OpenAI in 2023 was a tender/secondary transaction at an approximate $27–$29 billion valuation, investing about $130 million, primarily buying old shares from employees and early shareholders (the fact that this was secondary, not primary, was repeatedly emphasized in later reports). At that time, ChatGPT had recently exploded, but OpenAI was far from its current infrastructure narrative. Regulation, governance structure, and business models were highly uncertain. This was a “typical early-stage, high-uncertainty chip.”

Early 2024: $86B Employee Tender — Contrarian Accumulation During Governance Turmoil

At the end of 2023, the board ousted Altman, and a governance crisis erupted; theoretically, the valuation should have been discounted. However, in early 2024, the employee secondary sale led by Thrive still closed at an approximate $80–$86 billion valuation (reported by NYT as “$80 billion or more”), with a secondary scale of about $6.6 billion, confirmed by reports from NYT, CNBC, etc. For Thrive, this was a classic case of “bottom-fishing during chaos while still offering a much higher price than the previous round”: the risk premium was reflected in the terms and counterparty panic, rather than a massive nominal valuation discount.

September 2024: $6.5B Convertible Debt — Using Structural Tools to Lock in a Low-Price Cap

In September 2024, Reuters reported OpenAI was raising a $6.5 billion convertible debt round, and specifically noted: OpenAI offered Thrive a “sweetener” that other investors didn’t get, including the right to invest additional funds and a better conversion structure. The keys to convertible debt are:

Downside: interest + discount + protection clauses;

Upside: converting to equity at a pre-agreed price or discount under certain triggering conditions.

In other words, the nominal valuation didn’t look “that cheap,” but the risk-adjusted price was highly advantageous: if rounds at $280 billion, $300 billion, or even $500–$800 billion appeared later, Thrive could use lower, pre-locked terms to acquire more shares.

October 2024: $6.6B Primary Financing, Valuation $157B (Correcting Previous Market Valuation Illusions)

In the fall of 2024, OpenAI completed a $6.6 billion primary funding round, and the official valuation at the time was $157 billion. Although in the subsequent year of 2025, driven by surging secondary market sentiment, asking prices in some informal trades were hyped or even called at higher numbers, this $157B was the solid, official pricing anchor that laid the groundwork for the subsequent valuation spike.

April 2025: SoftBank Leads $40B Primary, Valuation ~$300B

Multiple media reports: In April 2025, SoftBank and other investors led a $40 billion primary round, pushing OpenAI’s valuation to nearly $300 billion. This round began to be seen as “the formation node of the AI hyperscale infrastructure story.” By this time, the chips from the previous $27B, $86B, and $157B milestones had already multiplied on paper.

December 2025: OpenAI Reverse-Invests in Thrive Holdings — Formation of a Circular Holding Structure

In December 2025, OpenAI announced taking an equity stake in Thrive Holdings. The two parties exchanged research capabilities for equity, using acquired traditional service companies as vehicles for AI implementation: accounting, IT outsourcing, professional services, etc. The essence of this structure is: capital + operations + technology cross-holding, deeply binding the interests of OpenAI and Thrive.

Early 2026: Middle East $100B Scale / Over $830B Valuation Negotiations; Thrive’s $285B Valuation Deal Exposed

Starting in 2026, market news indicated: the new capital Altman is seeking in the Middle East could reach a scale of $100 billion, with a target valuation of over $830 billion—one of the largest private rounds in global history. Concurrently, WSJ and CNBC reported: Thrive’s recent purchase was buying about $1 billion in shares in a secondary round at an approximate $285 billion valuation.

Connecting this timeline, you will find: Thrive was not a “stroke of sudden genius,” but a snowball rolling from $27 billion all the way to $285 billion, making it look incredibly cheap against the current narrative of over $800 billion. The real advantage comes from: being early, being bold, having complex structures, and mutually binding with OpenAI, rather than getting a “discount no one else got” in the current round.

III. Why Was Thrive Able to Get the “Low Price” in This $285B Valuation Round?

Breaking down the sources of this “cheapness” structurally, it roughly comes from four areas: transaction type, term privileges, strategic position, and the undeniable hidden leverage.

1) This is a Secondary Round, Not Competing for the Same Ticket as Sovereign Funds

The Middle East round of over $800 billion is primary: the company issues new shares, money goes into the company, used for hundreds of billions of dollars in compute and infrastructure investments over the coming years. Thrive’s $285 billion valuation buy-in comes from old shareholders/employees’ secondary:

Sellers care more about locking in the massive paper gains of the past 2-3 years than pressing for double the valuation;

The transaction scale is far smaller than $50 billion, so the company and major shareholders are willing to use a “slightly lower valuation + fast execution” to get it done;

These types of internal matching often carry a “relationship price,” prioritized for long-term investors deeply involved in governance.

2) Thrive Made Itself the “Only Buyer Eligible for This Price” via Structures like Convertible Debt

In the 2024 $6.5 billion convertible debt, Reuters disclosed: OpenAI gave Thrive “sweeteners,” including the right to invest additional funds and a better risk-reward structure relative to other investors.

Simply put: It’s not that “they bid lower than others,” it’s that “others have no right to bid at all.” The prices and rights were already pre-written in the convertible debt and shareholder agreements of previous rounds.

3) Strategic Position: Thrive is Not an Ordinary Financial Investor, But an “Operating Partner”

Thrive built Thrive Holdings, specifically to acquire accounting, IT, and professional service companies, embedding OpenAI’s model capabilities to do an “AI-version PE roll-up.” This brings OpenAI an exclusive enterprise GTM (Go-To-Market) channel and rapidly validates product forms in real-world business. When a shareholder can bring product implementation + acquisition platform + long-term synergy, the company is naturally willing to give a bit of a “partnership discount” on valuation.

4) Hidden Leverage and Omitted Risks: Family Background and “Survivorship Bias”

We cannot detach from reality and only talk about “perfect operational execution.” The Kushner family, behind Thrive founder Joshua Kushner, has incredibly deep roots in US political and business circles. During critical moments, such as OpenAI’s board turmoil or facing antitrust scrutiny, these top-tier political and business resources are often the hidden leverage needed to secure exclusive convertible debt terms that “others have no right to bid for.”

Furthermore, Thrive’s “god-tier moves” are accompanied by macro risks that cannot be ignored: if the regulatory pressure on OpenAI suddenly intensifies, if the ROI of AI infrastructure spending remains elusive, or if the “AI bubble” bursts, Thrive’s deeply bound “sink or swim together” approach will equally turn into a catastrophic chain reaction.

The essential answer: Because they spent three years first writing themselves into the terms with early capital and convertible debt, and then writing themselves into OpenAI’s business with an operating platform, all while being escorted by a formidable family background. By the time the $800 billion narrative emerged, this $285 billion price was already a pre-locked result in earlier contracts, not an improvised “super discount” negotiated on the spot.

IV. Thrive’s Other AI Portfolio: An “OpenAI Core” Driving Three Layers of Leverage

Finally, taking a quick scan of Thrive’s AI portfolio makes it easier to understand why they are willing and able to roll such a massive snowball on OpenAI.

Core Models and Infrastructure

OpenAI: The flagship holding, spanning $27B → $86B → $157B → $300B → adding more in the $285B secondary round → pursuing over $800B today.

Databricks: Data + AI platform, the data foundation that must be connected when bringing models to the enterprise side. Multiple analyses of Thrive’s new fund list Databricks as a core holding.

Cursor: AI code editor/IDE, sticking directly to developer productivity, seen as Thrive’s representative bet in “developer tools + AI.”

Anduril: Defense AI, turning AI into one of the operating systems for US defense through unmanned systems, command, and perception software.

Thrive Holdings: Embedding OpenAI into Traditional Services

Focused on acquiring accounting, IT, and professional services companies, using OpenAI for intelligent transformation, with OpenAI reverse-holding equity. This forms an “AI version of Berkshire + Accenture” combo: acquiring service companies with stable cash flows but lagging digitalization, then using models to boost profit margins and valuations.

Long-Term Underlying Assets

Holdings like SpaceX and Stripe, which have been mentioned multiple times, are themselves the hard infrastructure of the AI era (Starlink communication foundation) and the financial foundation (payments + risk control), providing “physical + financial” support for upper-layer AI workloads.

From an investment logic perspective, Thrive is not “casting a wide net to buy a bunch of AI apps,” but building a capital + operations flywheel centered around OpenAI:

Upstream: Betting on models and data infrastructure (OpenAI, Databricks);

Midstream: Deep integration using OpenAI (Cursor, Anduril);

Downstream: Directly operating traditional companies amplified by AI through Thrive Holdings.

This is why, when the market started talking about a valuation of over $800 billion, Thrive was no longer holding just one or two rounds of “financial tickets,” but a comprehensive “structured long-term position” filled with rights clauses and business synergies. Naturally, they could continue buying at a seemingly outrageous price of $285 billion while others were still queuing up to enter.