The Intelligence Layer Problem: Palantir’s True Boundaries as a Systems Integrator

Just hours ago, Michael Burry posted a tweet that pinpointed a structural collision the market has largely ignored. Burry noted that OpenAI’s newly launched “Frontier” system is explicitly defined as a “semantic layer for the enterprise.” Furthermore, OpenAI is dispatching its own “forward-deployed engineers” in alliance with external consultancies (like Accenture and McKinsey) to rewire enterprise workflows and integrate AI agents directly.

Burry astutely pointed out: “This sounds more than familiar. $PLTR somehow kept its name out of this story.”

This is not a mere overlap in business models; it is a direct superimposition occurring at the foundational level of the tech stack. Currently, the market—buoyed by Palantir’s robust Q4 2025 earnings showing a 137% surge in U.S. commercial revenue—has awarded the company a staggering ~70x trailing price-to-sales (P/S) multiple. Investors are pricing Palantir as an irreplaceable AI platform. However, stripping away the market mania to examine recent supply chain dynamics and underlying technical structures reveals that Palantir is facing an asymmetric, top-down threat.

1. The Supply Chain Reality Check: “Brains” vs. “Pipes”

A recent standoff over model control has brutally exposed Palantir’s actual position within the AI supply chain.

Anthropic CEO Dario Amodei formally rejected the U.S. Department of War’s ultimatum, refusing to lift safety guardrails that prevent its Claude model from being used for mass domestic surveillance or fully autonomous lethal weapons. In response, the military threatened to invoke the Defense Production Act and label Anthropic a “supply chain risk.” Concurrently, OpenAI and xAI agreed to the military’s standards, with xAI’s Grok already cleared for classified systems.

The structural takeaway here is cold and clear: When Anthropic faces removal from military networks to be replaced by Grok, Palantir—providing the “pipes” but not the “brain”—has no leverage over which model stays or goes.

Palantir possesses formidable deployment barriers (e.g., IL6 clearances, deep integration into defense programs), which constitute its “Deployment Sovereignty.” But it does not possess “Intelligence Sovereignty.” If the underlying reasoning engine is severed or swapped, Palantir’s platform cannot generate intelligence on its own; it defaults back to its true nature: a highly secure systems integrator.

2. The Objective Compression of the Ontology Layer

In the post-foundation model era, the bedrock of Palantir’s commercial moat is shifting.

Historically, Palantir’s core value resided in the ontology layer: the capability to ingest siloed, messy data and map it into a coherent semantic structure. But with Large Language Models (LLMs) natively possessing advanced reasoning and retrieval capabilities, this value chain is compressing:

Pre-LLM Stack: Raw Data -> Ontology Layer (Palantir) -> Custom ML -> Dashboard

Post-LLM Stack: Raw Data -> Retrieval -> Foundation Model (OpenAI/Claude) -> Agent Interface

By explicitly defining Frontier as an “enterprise semantic layer,” OpenAI signals that when models can directly ingest unstructured data and execute cross-node reasoning, the indispensability of bespoke ontology tools in the commercial mid-market and enterprise knowledge work sectors is drastically diminished.

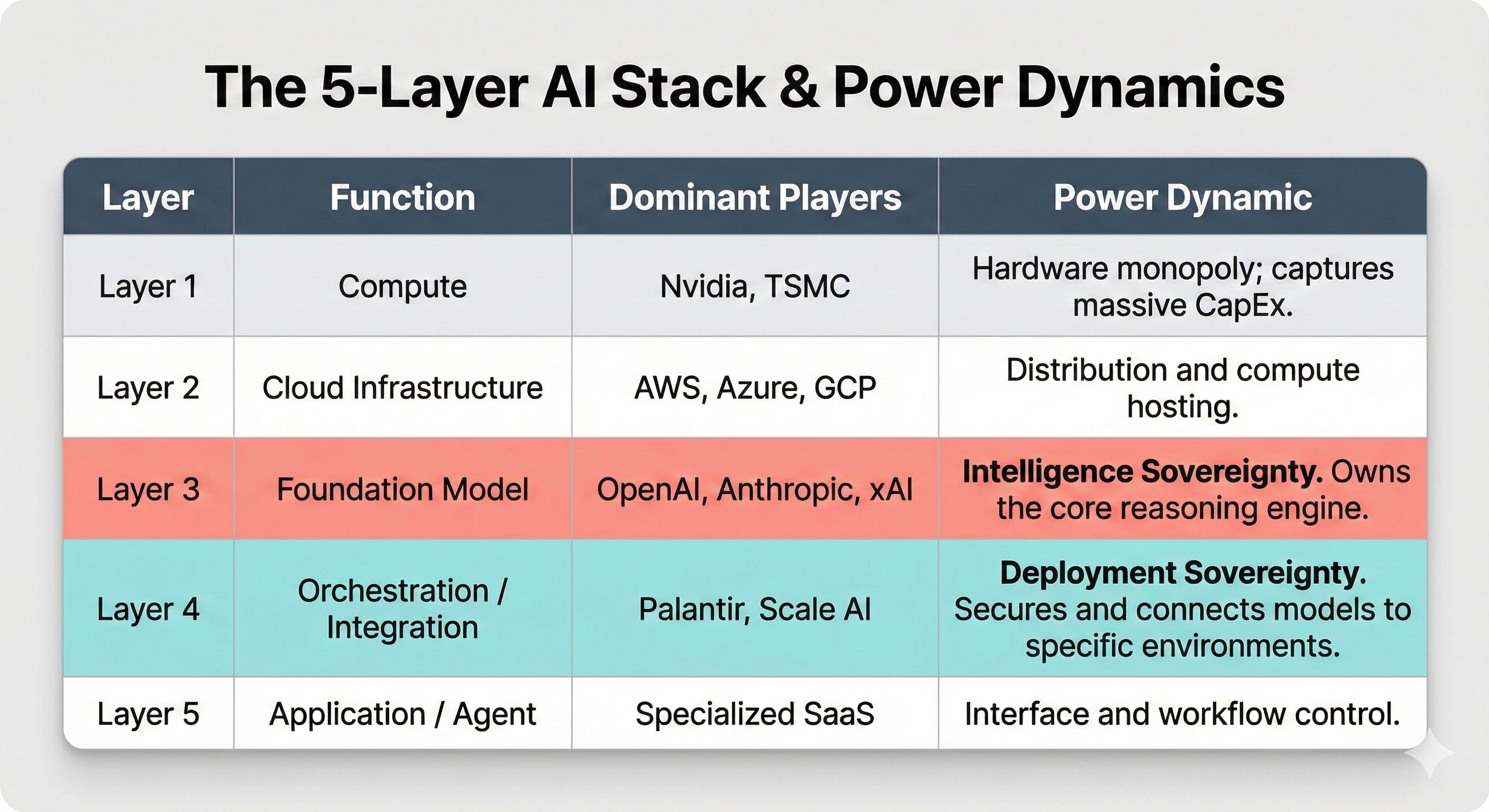

3. The 5-Layer AI Stack and Capital Mismatch

To understand the essence of this dynamic, we must map the actual power hierarchy of the AI ecosystem:

The core of Palantir’s valuation risk lies in capital mismatch: Palantir is a Layer 4 company being priced by the market with a Layer 3 (or even monopoly) premium. A 70x P/S multiple requires flawless, exponential commercial expansion—the exact territory that Layer 3 incumbents are now aggressively invading.

4. Asymmetric Competition: Deconstructing the Commercial Narrative

This brings us back to the ultimate commercial threat implied by Burry’s tweet. The crown jewel of Palantir’s Q4 2025 report was its robust commercial customer growth (totaling 954 clients). Yet, this is the precise target of OpenAI’s “Frontier Alliances.”

By launching Frontier and partnering with consultancies like Accenture to supply “forward-deployed engineers,” OpenAI has already secured early enterprise adopters like Intuit and Uber. This service model perfectly replicates Palantir’s commercial structure (Model Brain + Implementation Deployment), likely with unit economics that are highly attractive to corporate clients.

This is an asymmetric competition. OpenAI can extend downstream to build internal ontology tools and enterprise semantic layers. Palantir, however, cannot pivot overnight and deploy tens of billions in CapEx to train a frontier foundation model.

The Capital Reality

In the AI era, the ability to capture economic surplus across the tech stack is dictated by indispensability. Palantir’s “Deployment Sovereignty” within defense and hyper-secure compliance networks remains robust, but the steady growth of that sector cannot justify its hyper-inflated commercial valuation.

As the foundational players who own the “brains” begin building their own enterprise semantic layers and deployment channels, investors must coldly ask: What is the true boundary of a commercial premium for a systems integrator that only rents its intelligence?