The Valuation Scaffold: How SpaceX’s Belief-Based Valuation Entered the Public Market

The loudest question surrounding SpaceX’s IPO has been whether a two-trillion-dollar valuation is justified. But that may be the wrong question entirely. For a company like SpaceX, there has always been a vast temporal gap between current financials and market valuation — today’s revenue and profit figures simply cannot explain the price tag. The price rests instead on a future technology trajectory, industrial dominance, founder credibility, and the capital market’s capacity for imagination.

The more productive question, then, is not whether investors “believe” — it’s this: what kind of market structure allows a valuation so heavily dependent on future narrative to enter the public market and hold together in the early days after listing?

This piece calls that structure the “Valuation Scaffold.” It refers to the full set of external mechanisms — low float, governance insulation, price-insensitive buying, rapid index inclusion, derivatives amplification, and credit market support — that allow a company whose value rests primarily on narrative, founder credibility, and technological imagination to hold up its public market valuation in the period before genuine, broad-based price discovery has taken place.

A scaffold doesn’t prove that a building is sound. It provides temporary support while the building has yet to face its final test. In capital markets terms, a valuation scaffold doesn’t prove the company is worth the price — it simply allows the company to establish a tradeable, transmittable, partially index- and credit-market-endorsed price platform before it has to face a wider and more price-sensitive pool of capital.

This structure is not unique to SpaceX. SpaceX is simply the most complete example we have seen assembled to date. Understanding how it works matters more than debating whether SpaceX “deserves” its valuation — because this same structure is about to shape how an entire cohort of similar companies enters the public market.

I. Low Float: Engineering Artificial Scarcity

SpaceX’s public float sits between 4% and 5%, with more than 95% of shares locked up.

This is not an organic byproduct of the listing process — it is a deliberately engineered parameter. State Street (SSGA), in its institutional research, has noted that founder-led mega-cap companies with strategic control ambitions have historically tended to list with lower initial floats, allowing them to complete the capital raise and listing while minimizing dilution of control and short-term market disruption. Float size, like pricing range and lock-up terms, is a variable to be decided when structuring an offering.

The effect is mathematical. When only 4% of shares can trade, the market only needs a small cluster of marginal buyers to agree on a price — and that price is then extrapolated outward as the implied valuation of all 13.1 billion shares. In other words, what the market is actually pricing is the marginal price of a thin slice of tradeable shares, not a direct assessment of the company’s total value.

II. Governance Decoupling: Price Is Tradeable, Control Is Not

SpaceX has a dual-class share structure. Post-IPO, Musk holds approximately 42% of the economic interest but controls roughly 82% of the voting power through Class B shares.

This means the public market has no institutional mechanism to meaningfully constrain the company — no realistic prospect of a proxy fight, no threat of board reconstitution, no path to a hostile takeover. The only lever available to public investors is the right to buy and sell that 4% float, which exerts no structural influence over the company’s capital allocation or strategic direction.

This point and the low-float design are two sides of the same logic: float determines how many chips the market gets to play with; voting structure determines whether those chips can be exchanged for any real governance power. Within this framework, “going public” functions more as a liquidity event than a redistribution of control.

III. Buyer Composition: Who’s Buying Determines How Price-Sensitive the Buying Is

The composition of buyers directly shapes what kind of demand that 4% float actually faces.

SpaceX’s original plan was to allocate up to 30% of IPO shares to retail investors — well above the industry norm of 5–10% — and the actual first-day retail allocation exceeded 20%. This was an active distribution choice made by the underwriters.

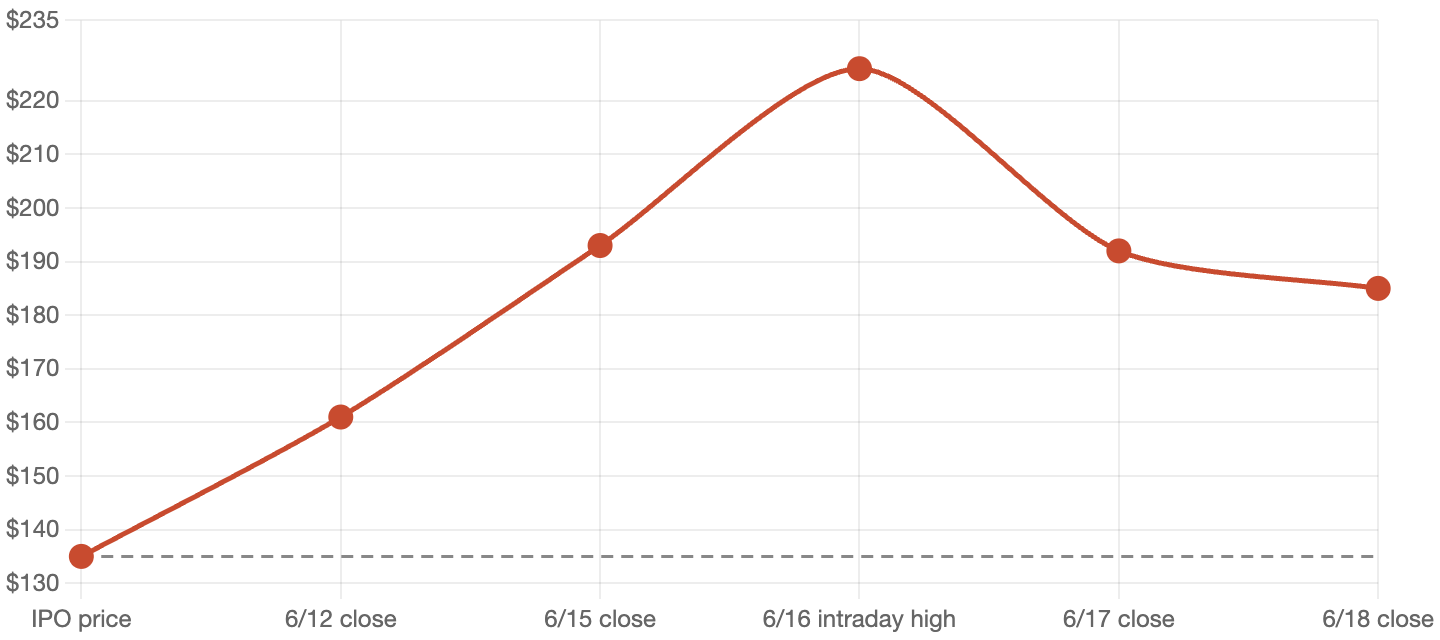

At the same time, in the first days of trading, virtually no shares were available to borrow for short selling, and options on SPCX did not begin trading until the third day (June 16). In other words, during the most critical window for price discovery, the market structure only allowed one form of expression: bullishness. The moment that constraint began to ease, the stock experienced its first meaningful pullback since listing — a timing that is hard to dismiss as coincidental.

Within days of the IPO, eleven leveraged ETFs tracking SPCX launched, along with 24/7 perpetual futures contracts on platforms like Hyperliquid. These products added no new shares to the actual float; they layered synthetic, leveraged demand on top of an already thin supply of real shares.

Each of these developments has its own commercial rationale — underwriters cultivating retail relationships, options exchanges approving new listings on their own schedule, ETF issuers chasing a hot product. But their cumulative effect was consistent: in the early window when prices are most susceptible to being “set,” the share of price-insensitive capital was systematically enlarged, while the corrective forces of price-sensitive capital — short sellers, hedge funds, options markets — were structurally delayed.

One distinction deserves emphasis here, because it is frequently misunderstood: when index funds buy in (discussed next), they are not endorsing the valuation — they are following rules.

Taken together, the low float (Part I) and buyer composition (Part III) form the technical core of the valuation scaffold: what might be called a “Float Leverage System.” A small pool of genuinely tradeable shares, amplified through retail overweighting, index inclusion mechanics, derivatives leverage, and passive fund rules, is multiplied into a public market valuation for the entire share count.

IV. Index Rules: Turning Scarcity into an Automatic Mechanism

According to public reporting, the NYSE and Nasdaq competed for SpaceX’s listing in March 2026. Reuters, citing sources familiar with the matter, reported that SpaceX made “rapid inclusion in the Nasdaq 100” a core condition for its exchange selection. Nasdaq subsequently compressed the waiting period for large-cap new listings from three months to fifteen trading days and eliminated the 10% minimum float requirement. The Russell indices moved even faster, reducing their window to just five trading days. These rule changes will apply to future listings by companies like OpenAI and Anthropic as well — but objectively, they make it easier for low-float, mega-cap newcomers to enter the passive fund universe quickly.

The weighting formula amplifies this further. Under the new Nasdaq rules, companies with lower floats have their index weights calculated at a multiple of their actual float — up to three times the real float ratio. For SpaceX, a real float of roughly 4.3% translates into an index weight calculated as if the float were approximately 12.9%. Some observers have called this a “ghost market cap” effect: passive funds are required by rule to buy as if a far larger share of the company were freely tradeable, even though the actual available supply has not increased correspondingly. This is a structural liquidity mismatch — rule-mandated purchase obligations that exceed what the market can actually deliver.

Across multiple institutional estimates, mechanical index buying from this round of inclusions is expected to total roughly $20–30 billion in near-term demand. If the S&P 500 follows suit — currently not expected until mid-2027 at the earliest — that would add over $50 billion in additional passive demand.

The S&P 500’s stance offers a useful counterpoint. The index’s committee discussed whether to relax its criteria earlier in 2026 but ultimately confirmed on June 4 that it would maintain the 12-month seasoning period and GAAP profitability requirement, meaning SpaceX would not be eligible for S&P 500 inclusion until mid-2027 at the earliest. This demonstrates that accommodating low-float mega-caps is not a universal index industry position — different institutions have made different trade-offs.

This index rule environment is not unique to SpaceX; it is a structural feature that an entire pipeline of companies will encounter. According to research by NEPC and MSCI, the ten highest-valued venture-backed private companies today represent roughly $3 trillion in equity value — approximately 5% of the S&P 500’s current total market cap. OpenAI, Anthropic, Databricks, and Stripe are all on that list. If these companies come to market via similar low-float structures, SpaceX will likely serve as their primary reference template — though that remains a trend extrapolation, not a certainty.

V. Credit Markets: The Support Structure Extends Beyond Equities

Less than a week after listing, SpaceX received investment-grade ratings from all three major agencies — Fitch, S&P, and Moody’s (BBB+/BBB/Baa1) — and promptly moved to launch a bond offering of at least $20 billion. This occurred while the company posted a combined operating loss of $1.943 billion in the first quarter, remained deep in a capital expenditure cycle, and had yet to show profitability in its AI-related ventures.

The willingness of credit markets to assign investment-grade ratings under these financial conditions suggests that SpaceX’s capital market narrative is reaching well beyond equity investors. For fixed income investors, Starlink’s relatively stable cash flows, the scale of the asset base, and the founder’s demonstrated ability to continue raising capital may together provide enough offset to near-term losses — this is a fairly conventional credit analysis framework, not a case of rating agencies being “talked into” a story. But it does mean that the scaffold doesn’t only exist in the equity market; it extends into the credit market, which is supposed to weight cash flow and leverage metrics more heavily.

What This Structure Is Actually Doing: Creating Value, or Deferring Price Discovery?

Viewed together, these five elements point toward a question more worth asking than whether SpaceX “deserves” a two-trillion-dollar valuation: is this structure helping the market price a genuinely promising company more accurately, or is it systematically deferring a real price discovery process that should happen — and eventually will?

The structure excels at one specific task: manufacturing a spectacular IPO debut, and maintaining the appearance that “the market has validated the story” for as long as lock-up periods hold. But each of its components objectively shapes who gets to participate in price formation during the critical early window — retail investors, passive funds required by rule to follow, a market structure that temporarily lacks short-selling tools, and credit agencies willing to apply conventional analytical frameworks.

None of this changes the company’s underlying fundamentals. What it changes is who gets to price the company first. This is the structural outcome the valuation scaffold produces: a “Pricing Priority Structure” in which price-insensitive, rule-constrained capital enters the price formation process first, while more skeptical, cash-flow-focused capital is pushed to the back of the queue — to be heard only after float expands and short-selling tools mature.

And the scaffold has an expiration date. Within the next 90 days, approximately 2 billion shares — more than three times the current float — are set to be released from lock-up. Short-selling and options tools are already in the market. The capital flows into leveraged ETFs and perpetual futures contracts can reverse. And the S&P 500 — a gate that remains closed for now — will eventually have to be reassessed. As these constraints lift one by one, and the float normalizes toward typical levels, the price will no longer be set by this early-stage structure. It will be set by the wider, more price-sensitive capital waiting further down the queue.

Closing

SpaceX’s first week of trading does not prove that the building stands. What it actually demonstrates is that capital markets have developed a remarkably sophisticated valuation scaffold for belief-driven mega-companies — one capable of holding up a price before that price has been tested by a full market. Low float and buyer composition form its technical core (the Float Leverage System); index rules, retail allocation, and credit ratings institutionalize it (the Pricing Priority Structure).

The scaffold has not eliminated price discovery. It has changed the sequence — ensuring that the first capital to set the price is not the most cautious or most price-sensitive, but the most narrative-receptive, the most rule-bound, or the most eager to participate. The real test will come when the float expands, lock-ups expire, short-selling matures, and earnings cycles unfold — in other words, when the scaffold comes down, and the building has to hold itself up.

SpaceX is therefore not an isolated IPO story. It is a template. The real question is not what price the market put on this company in its first week — it’s what structure is underneath that price, when it starts to come apart, and what remains when it does.