Three Roads to Autonomous Driving: Waymo, Tesla, and Nvidia

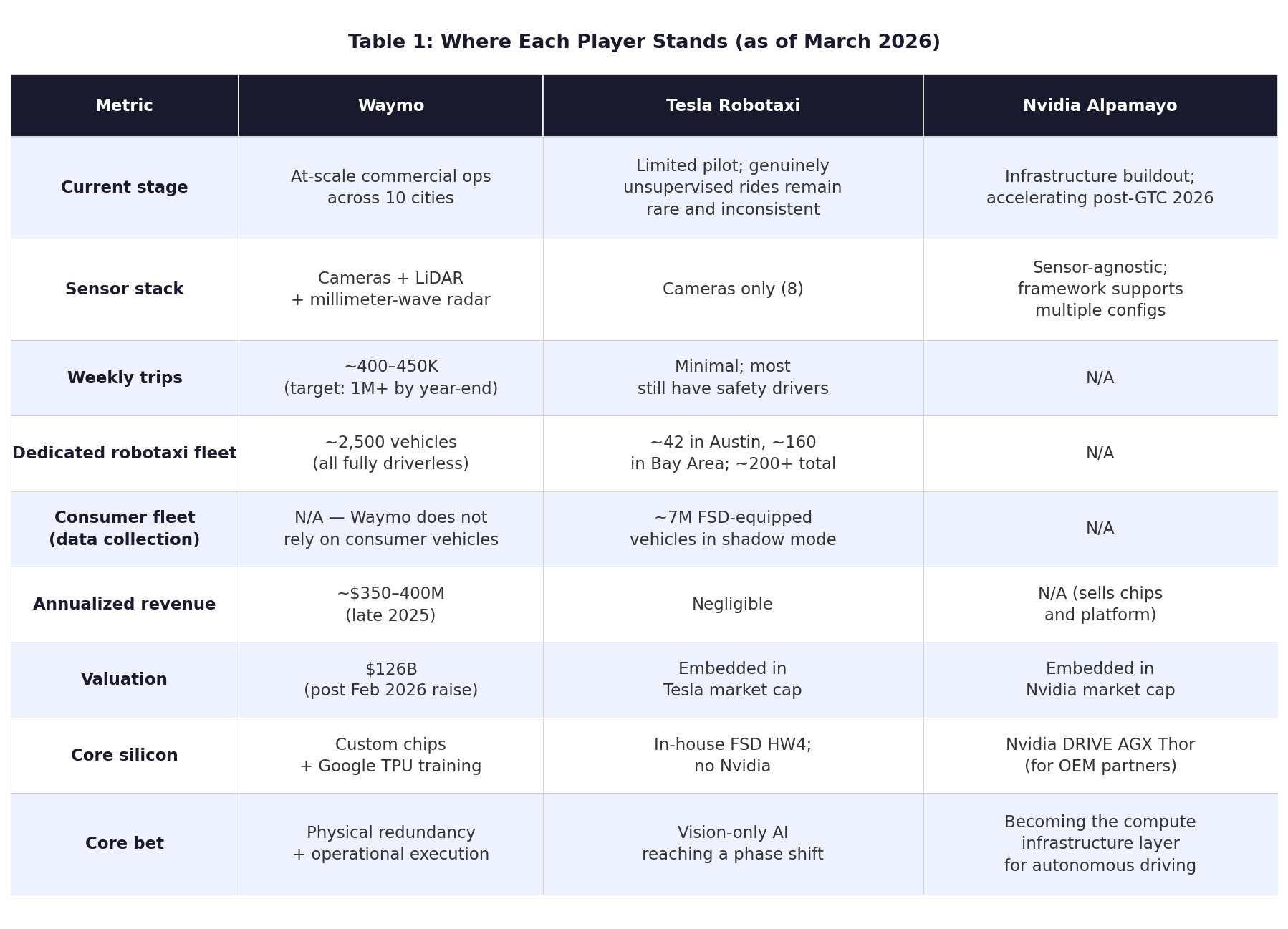

San Francisco, March 2026. A white Jaguar I-PACE with no one behind the wheel sits at a red light. In the back seat, someone has a laptop open. No safety driver, no one monitoring the wheel — and nobody gives it a second glance.

That same week, in Austin, a Model Y with a Robotaxi decal is taking fares. A safety officer sits in the passenger seat. One Tesla enthusiast made a point of riding 42 consecutive times — every trip had a safety officer. Another rider logged 58 trips before catching one that was genuinely unsupervised.

This is not a gap in scale. These are two things at completely different stages of maturity.

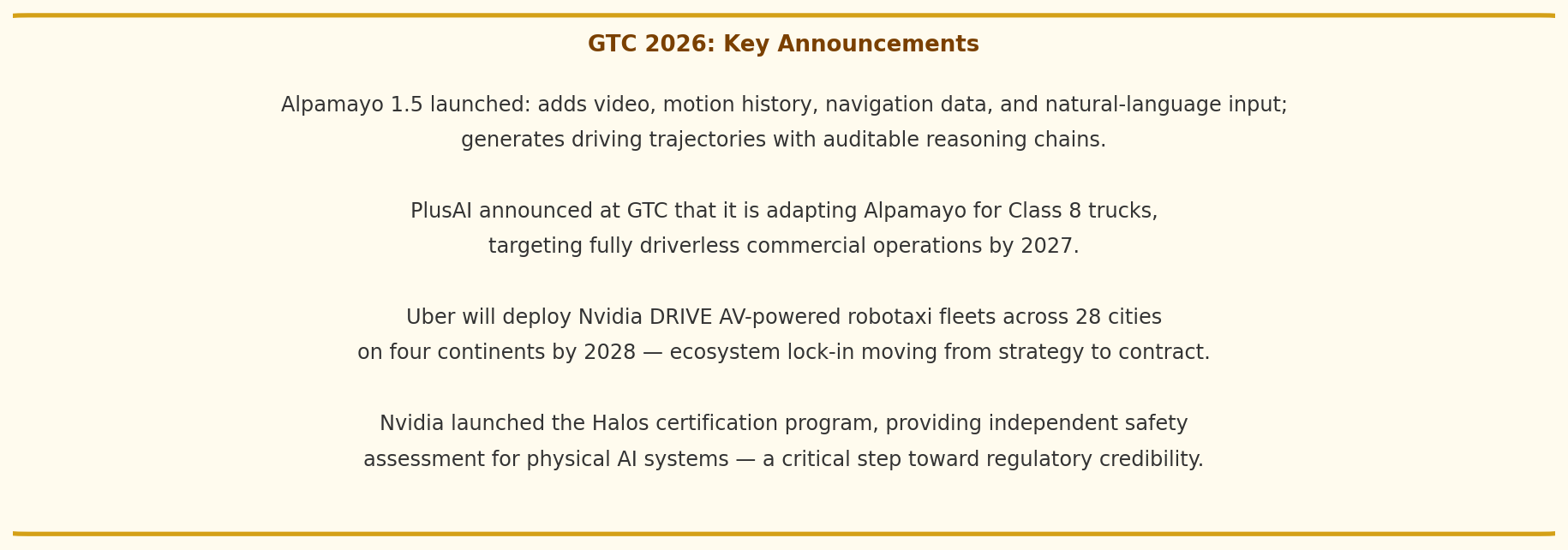

Then came GTC 2026. Jensen Huang rode through San Francisco in a NVIDIA DRIVE AV vehicle and took the stage to declare: the ChatGPT moment for autonomous driving has arrived. He announced BYD, Hyundai, Nissan, and Geely joining the platform; Uber deploying Nvidia-powered fleets across 28 cities on four continents by 2028; and Alpamayo 1.5 shipping that day.

Three players. Three distinct logics. Three fundamentally different roads. Treating them as variants of the same story is the most common analytical error in autonomous driving coverage.

I. The Current State of Play

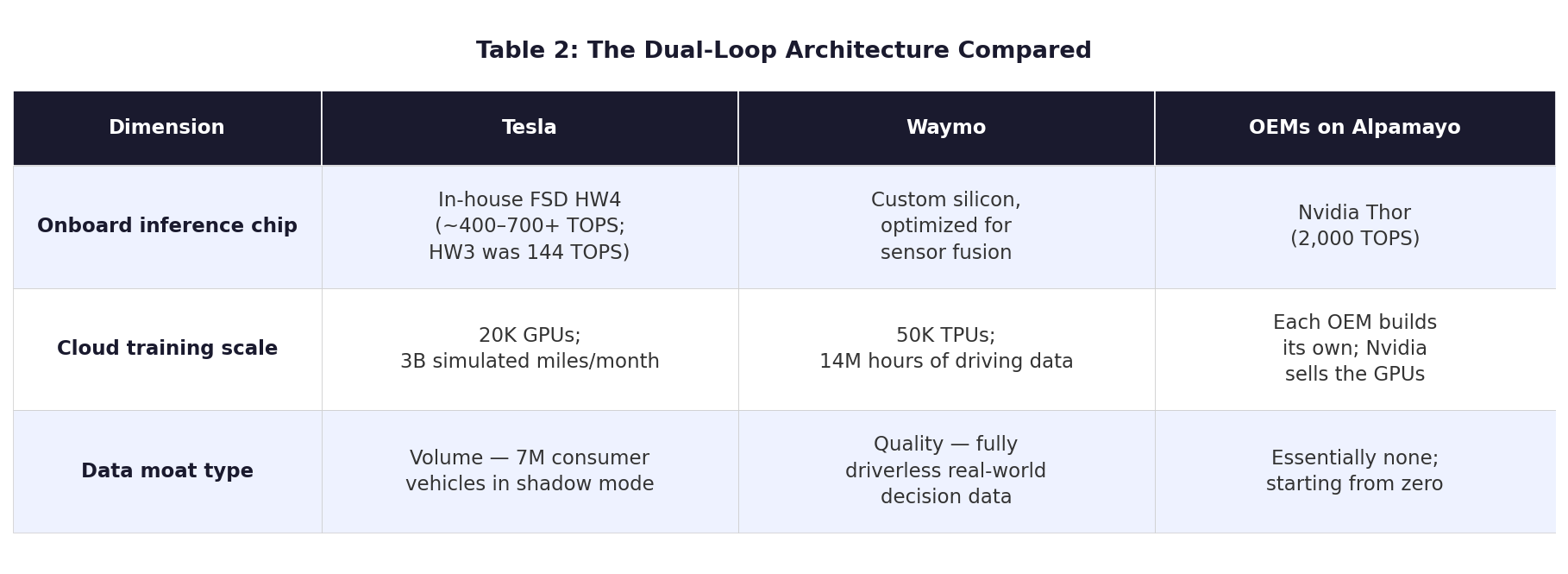

One detail worth isolating: neither Waymo nor Tesla is a meaningful Nvidia customer. Both have developed their own silicon and are deliberately routing around Nvidia.

Alpamayo’s real target customers are the legacy automakers — Mercedes, JLR, Lucid, BYD, Hyundai — that lack the capability to build their own chips. Nvidia has engineered a position where it wins regardless of which robotaxi operator ultimately prevails.

II. The Architecture Has Converged: All Three Run Transformers

Waymo, Tesla, and Nvidia’s Alpamayo all run on Transformer architecture.

A Transformer is not fundamentally a language model — it is a general-purpose relational modeler for any sequence. Language is a sequence of symbols; video is a sequence of frames; a driving scene is a sequence of multi-modal sensor inputs. The underlying principle is the same across all three.

Tesla replaced over 300,000 lines of explicit C++ control code with an end-to-end Transformer in FSD v12.

Waymo’s EMMA research model is built directly on Google Gemini — a pure Transformer.

Alpamayo runs on Nvidia’s Cosmos-Reason, with a natural-language reasoning chain inserted between the visual encoder and the action decoder.

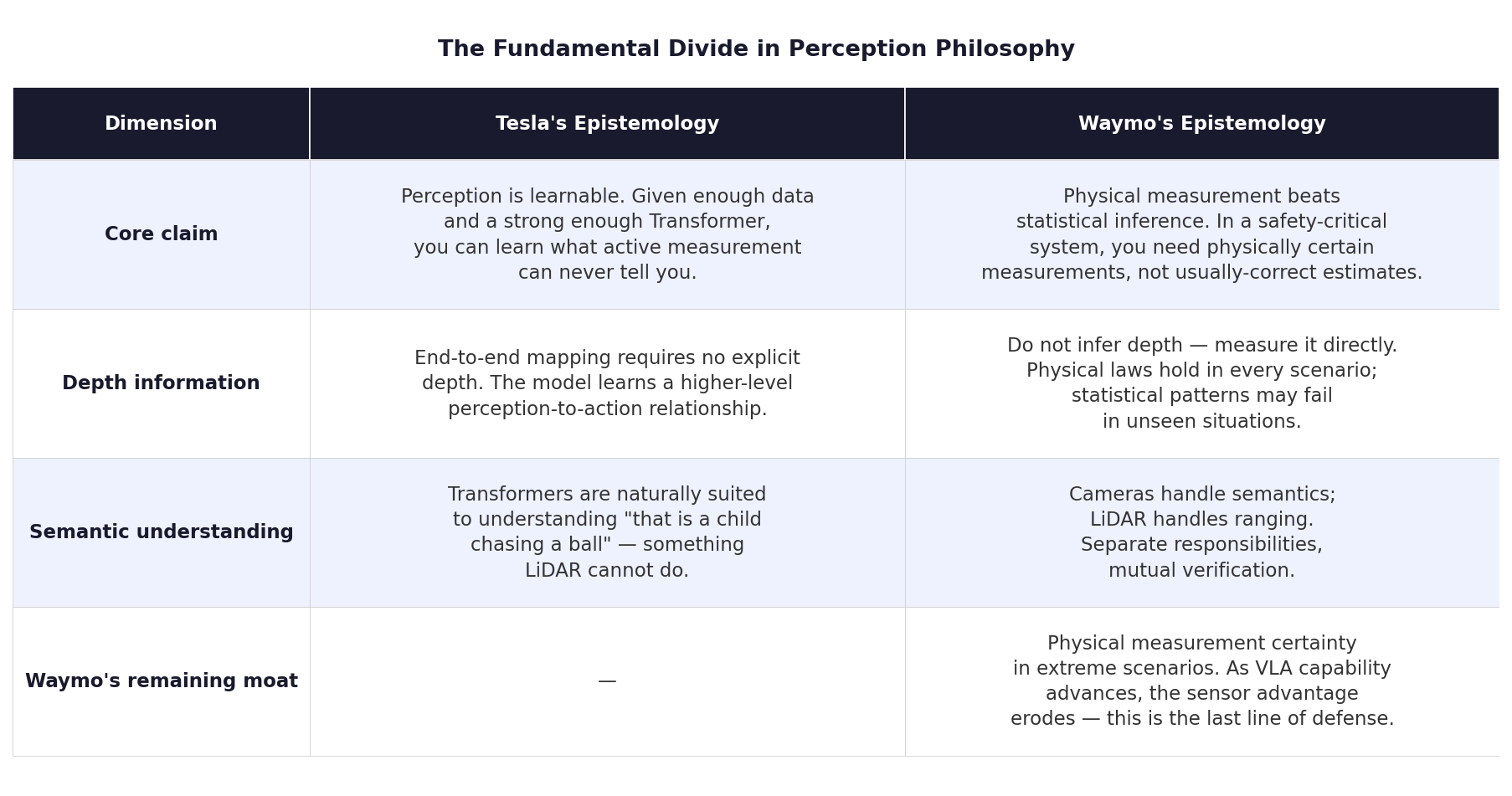

III. Cameras vs. LiDAR: A Debate That Has Never Been Properly Framed

Passive vs. Active Sensing

A camera is a passive sensor — it captures ambient light, sees color, texture, and shape with extraordinary semantic richness. What it cannot do is directly measure distance. Depth must be inferred through perspective cues, object size, and motion parallax. This is an inverse problem: reconstructing three dimensions from two, with inherent information loss.

LiDAR is an active sensor. It fires laser pulses and measures return time, producing a precise 3D point cloud with exact XYZ coordinates for every point. No inference required — depth is physically measured. This is physics, not statistics.

The Deeper Issue Almost Nobody Gets Right

LiDAR knows there is an object 1.8 meters ahead. It does not know whether that object is a dog, a child, or a cardboard box.

That distinction matters enormously. A dog might bolt into the road; a cardboard box will not. A child chasing a ball might run into the lane; an adult typically will not. These behavioral semantics are invisible to LiDAR — they require cameras and semantic understanding to recover.

This is why Waymo has never been LiDAR-only. It fuses three sensing modalities: LiDAR for precise ranging and 3D localization, cameras for semantic understanding, and millimeter-wave radar for velocity. Each handles what it does best; all three cross-check each other.

Tesla’s end-to-end Transformer maps directly from pixels to actions — no explicit depth estimation step. What it has learned is the mapping from a visual scene to what a skilled human driver would do, implicitly encoding object type, behavioral intent, and scene semantics — including the things LiDAR cannot see.

IV. The Long Tail: This Is the Real Battleground

The distribution of driving scenarios is extremely skewed. The vast majority of driving time is spent in routine situations — open roads, traffic lights, standard lane changes. Models train easily on this material.

The long tail is where the hard problems live: a tree felled by a blizzard lying across the road; a construction zone that has temporarily reversed traffic flow; an intersection where every signal has gone dark; a pedestrian in an unusual costume; a vehicle traveling the wrong way; an ambulance approaching from an unexpected direction. Each has a low individual probability — but there are infinitely many of them.

The deeper difficulty: you cannot know what you do not know.

Tesla: Volume as the answer.

Millions of FSD-equipped consumer vehicles are generating data globally. The important distinction is between two fleets: the dedicated robotaxi test fleet (~200 vehicles in Austin and the Bay Area) and the consumer fleet (~7M FSD-equipped cars in shadow mode). Tesla’s data flywheel advantage comes from the latter. The trap is data quality — supervised FSD data and fully autonomous decision data have fundamentally different training value. Even the ‘unsupervised’ Robotaxi program, at one point, simply moved the safety officer from inside the vehicle to a following chase car.

Waymo: Quality over quantity.

Some long-tail scenarios occur so rarely that decades of real-world operation won’t yield enough ground truth — simulation is essential. But LiDAR’s physical measurements hold under any long-tail condition regardless of prior exposure. The 2,500 fully driverless vehicles in Waymo’s commercial fleet generate data of a fundamentally higher quality than Tesla’s millions of supervised consumer vehicles.

Nvidia Alpamayo: Reasoning as a substitute for coverage.

Alpamayo 1.5’s chain-of-thought reasoning is designed to let a vehicle work through an unfamiliar scenario step by step, rather than relying on having seen something similar in training. Musk’s counterargument is hard to dismiss: the framework is available, but the data is still your own problem.

V. Nvidia’s Alpamayo: Not a Model — an Infrastructure Layer

Alpamayo is a Vision-Language-Action Model ecosystem, not a deployable autonomous driving system. It is organized in three layers:

Foundation model: a 10B-parameter VLA pretrained on 80,000 hours of multi-camera driving data across 25 countries, open-sourced on Hugging Face — now the most-downloaded robotics model on the platform.

Fine-tuning toolchain: OEM partners train on their own fleet data to produce versions calibrated to their specific vehicle, environment, and sensor configuration.

Knowledge distillation: the 10B teacher is compressed into edge models small enough to run inference in milliseconds on vehicle hardware. PlusAI distilled a 10B teacher down to a 0.5B edge model for real-time inference on Class 8 trucks.

One further distinction: Tesla FSD is black-box inference — there is no accessible record of why the vehicle made a given decision. Alpamayo generates an explicit reasoning trace alongside every driving instruction: ‘I can see a double-parked vehicle ahead; there is oncoming traffic on the left; I am waiting for a gap before proceeding.’

That trace is auditable. It can be reviewed after an incident. As regulatory pressure intensifies, auditability is evolving from a technical feature into a commercial advantage.

VI. The Dual Loop: Real-Time Inference and Continuous Learning

All three approaches share a common computational structure. Understanding it is essential for assessing each company’s moat.

The inference loop (millisecond-scale, fully local): sensor input → onboard chip → driving decision → execution. No connectivity required. Safe decisions must complete within 10ms; even a 4G network adds at least 50ms of latency.

The learning loop (asynchronous, cloud-based): vehicle flags high-value clips → uploads to cloud → training set update → large model retrained → updated edge model pushed via OTA.

This structure reveals Nvidia’s actual strategic intent. It is not competing in the data war. But it sits at the mandatory chokepoint through which data becomes a deployed model.

Open-sourcing Alpamayo looks like generosity. Structurally, it converts compute dependency into ecosystem dependency — and ecosystem dependencies are much harder to replace.

VII. Two Qualitatively Different Types of Uncertainty

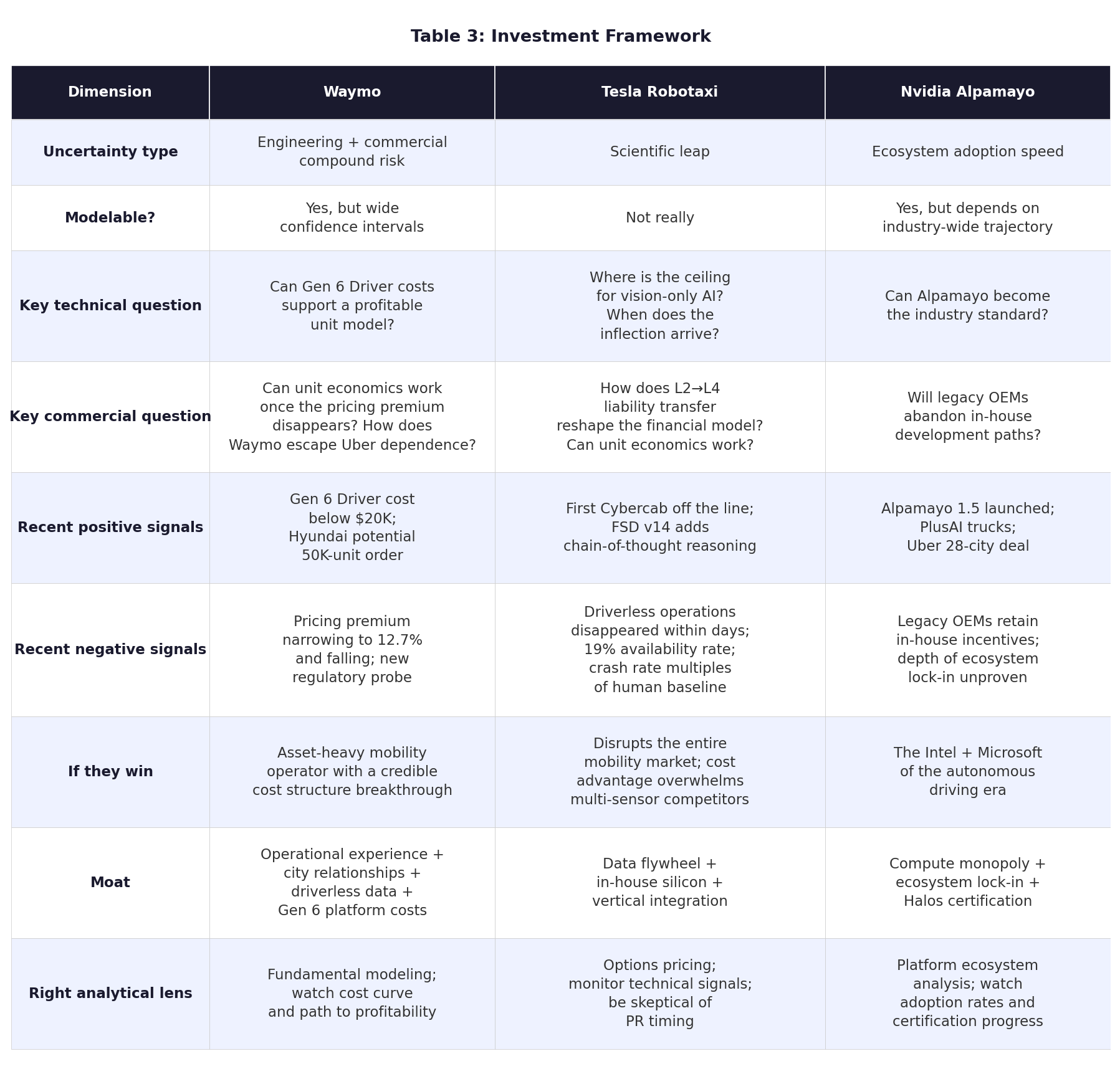

Waymo: Engineering Uncertainty — Modelable

Waymo’s core question is whether known things can be accomplished at the right time and the right cost.

The good news: the cost trajectory has genuinely inflected. Sixth-generation Waymo Driver costs are below $20,000 per vehicle on top of the base car — down more than 80% from fifth-generation’s $100,000+. Hyundai’s IONIQ 5 supply agreement, reportedly covering up to 50,000 vehicles, would be the largest vehicle procurement in autonomous driving history.

The bad news: the pricing premium is compressing. In June 2025, Waymo rides were priced 30–40% above comparable Uber trips. By end of 2025, that gap had narrowed to 12.7%. When the premium disappears entirely, the cost structure will be fully exposed to competitive pressure.

The strategic tension: Waymo is increasingly dependent on Uber and Lyft for passenger acquisition — gradually outsourcing pricing power, user data, and brand touchpoints to potential adversaries.

· · ·

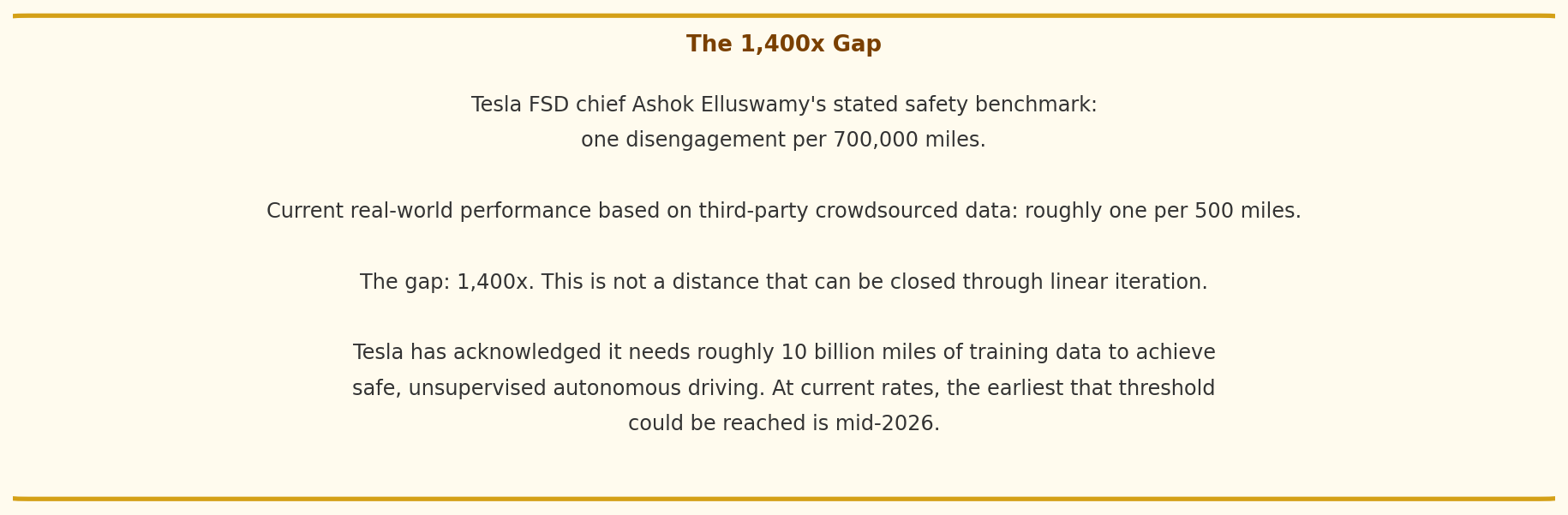

Tesla: Scientific Uncertainty — Essentially Unmodelable

Tesla’s core question: what is the upper bound on vision-only AI in the long tail of driving scenarios? This cannot be measured against milestones, because the finish line is unknown.

A recent episode made the uncertainty concrete. Two days before Tesla’s Q4 2026 earnings, the company announced unsupervised Robotaxi operations had begun in Austin. The stock jumped 4%. It subsequently emerged that ‘unsupervised’ meant the safety officer had moved from inside the vehicle to a following chase car. Within a week of the earnings release, even that limited operation had vanished from the tracking data.

Three readings of this pattern:

1. A people problem. Musk has a systematic optimism bias. The January 2026 announcement came two days before an earnings report — hard to call that coincidental.

2. A cognitive trap inherent to exponential curves. People inside rapidly improving systems systematically underestimate the remaining distance. Musk himself acknowledged in 2021 that generalized autonomous driving was ‘harder than I thought.’

3. A deliberate narrative tool. Optimistic timelines lead consumers to pay up to $12,000 for FSD subscriptions, sustain high valuations, and keep engineering teams motivated. Missing deadlines is not only a failure — it is a component of Tesla’s business model.

These readings are not mutually exclusive. They converge on the same investment conclusion: Tesla Robotaxi is an option with an entirely unknown expiration date.

VIII. The Overlooked Fourth Pillar: Liability and Unit Economics

Winning on technology does not mean winning in business.

L2 vs. L4: A Structural Financial Difference

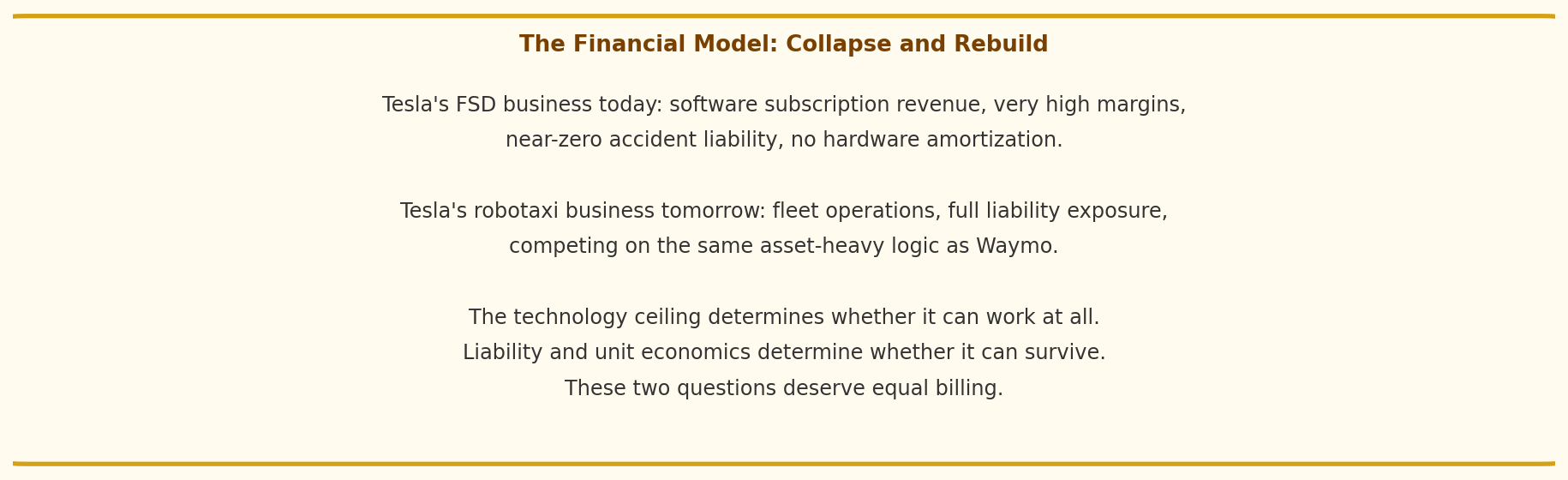

Tesla FSD today is L2. In an accident, liability belongs to the driver. Tesla sells high-margin software subscriptions while bearing near-zero accident liability: pure software revenue, zero hardware amortization, minimal legal exposure.

Tesla Robotaxi is L4. The moment Tesla operates genuinely unsupervised fleets, the liability structure transforms. Substantial insurance is required. The company shifts from a high-margin software business to a transportation operator bearing accident liability — and those two types of companies carry very different valuation frameworks.

Unit Economics: The Fundamental Arithmetic

Assume the technology works perfectly. Can a robotaxi business actually make money?

The relevant benchmark: Uber’s all-in cost per mile for a human driver is roughly $0.60–0.80. Robotaxi economics require getting total cost below that level.

Waymo sixth-gen back-of-envelope: Driver hardware below $20K + ~$45K IONIQ 5 = ~$65K per vehicle. At commercial intensity (~20 hrs/day, 15 mph average, 4-year life), total mileage is roughly 420,000 miles. Hardware amortization alone: ~$0.15/mile. Adding charging, remote monitoring, and insurance brings a rough total to ~$0.45/mile — approaching or below the $0.60–0.80 human driver baseline.

The sixth-generation cost structure is theoretically viable. The prior generation — at $100K+ for the Driver hardware — was not.

Tesla’s sensor cost advantage is real — vehicle costs are substantially lower than Waymo’s. But once you add L4 liability insurance, remote assistance staffing (Waymo operates a remote monitoring team in the Philippines — a cost that rarely appears in these analyses), and compute, whether the unit economics actually work remains genuinely open.

IX. Convergence Is the Destination

The vision-only vs. multi-sensor binary may be a false frame.

Waymo’s co-CEO said in a February 2026 Bloomberg interview that she does not rule out simplifying the sensor stack — if vision-only AI is good enough, Waymo has strong commercial incentives to remove some LiDAR and dramatically cut per-vehicle costs.

Meanwhile, Tesla’s Robotaxi is already operating within a geofenced area in Austin — a predetermined zone with prior mapping. Logically, this is not categorically different from the HD map approach Musk has repeatedly mocked as unscalable.

The likely long-run winner may be a hybrid: lightweight LiDAR + high-quality vision + chain-of-thought reasoning. The combatants on all sides may quietly move toward each other.

X. Investment Framework

Waymo

A modelable story with demanding execution requirements. Sixth-generation costs have genuinely inflected; unit economics are theoretically approaching viability. But the pricing premium is compressing, Uber dependence is a structural contradiction, and Alphabet’s long-term capital commitment is the largest variable in the model.

Tesla Robotaxi

An unmodelable story with potentially enormous upside, attached to a certain financial trap. The L2→L4 transition does not require an AI breakthrough — only a business decision to enter the market. Even if the technology succeeds, rebuilding the business model will take time and cost. Investing here is a bet on timing, not engineering.

Nvidia

A structural winner story. No position on which sensor stack wins. No need to pick a robotaxi champion. Real customers are legacy OEMs without the capability to build their own silicon. Post-GTC 2026, positioning has moved from strategy to contracts. The business logic is more durable than it appears.

Data as of March 21, 2026. Not investment advice.