When Trillion-Dollar AI Companies Go Public: How Much Growth Is Left?

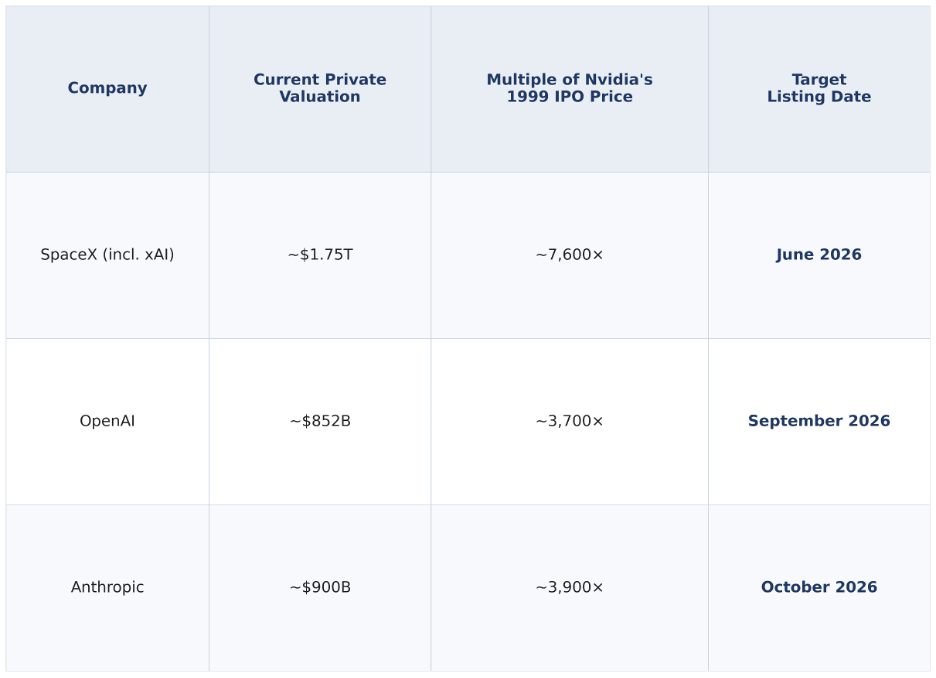

On May 20, 2026, SpaceX—having completed its merger with xAI in February—filed an S-1 with the SEC targeting a valuation of approximately $1.75 trillion, with a planned Nasdaq listing expected by late June. It would be the largest IPO in history. Two days later, OpenAI quietly submitted its own S-1, aiming for a September debut; Anthropic, meanwhile, has retained Wilson Sonsini to begin IPO preparations and is targeting an October listing.

Three of the most consequential AI companies in the world are heading to the public markets within the same autumn window. For investors, the question is deceptively simple: how much upside is actually left?

This is not an easy question—and answering it requires reading four decades of market history. More precisely, it is a question about alpha migration: over the past 40 years, the most significant value creation in the technology sector has been systematically shifting from the public markets to the private markets. The role of the secondary market investor has quietly changed—from early-stage risk capital provider to liquidity absorber for maturing assets.

1. The Data: Forty Years of Compressing Multiples

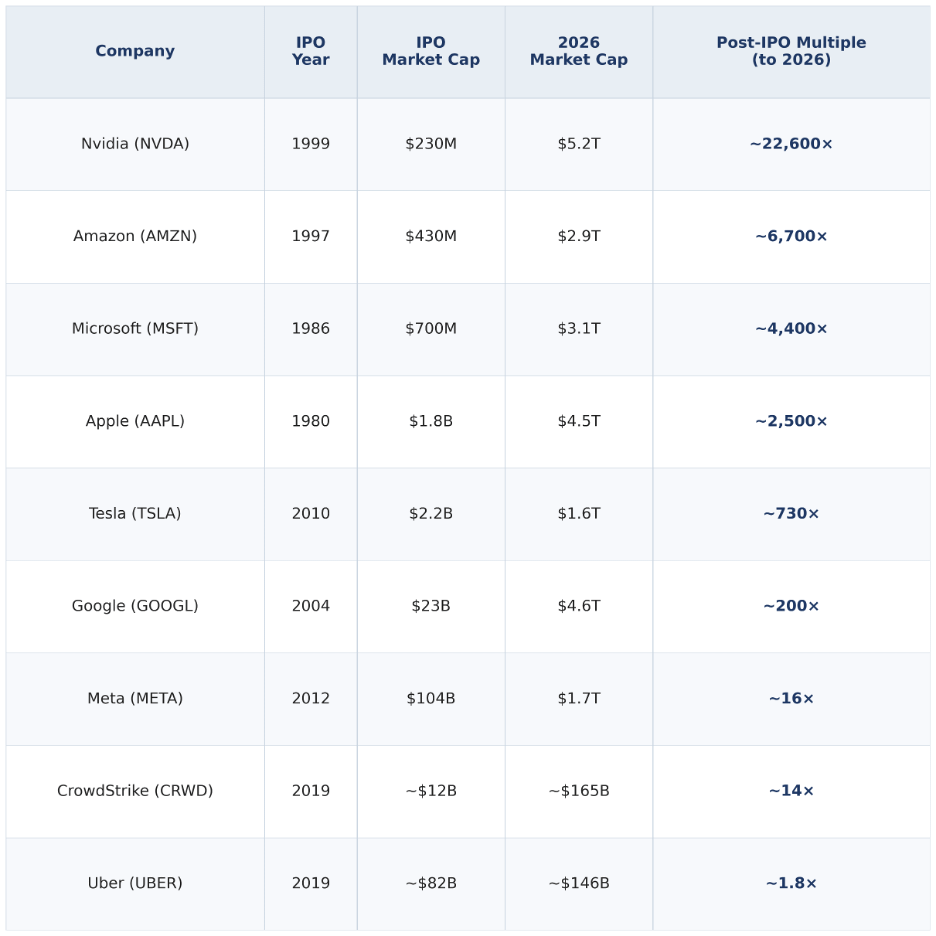

Over the past four decades, the multiple from IPO price to today’s market capitalization for major technology companies traces a clear downward curve.

The pattern across representative samples is unambiguous: companies are entering the public markets in an increasingly “pre-priced” state, and the early-growth runway available to ordinary investors is narrowing in a systematic way. This is not random variation. It is a traceable structural shift. (Note: figures in the table reflect companies that survived and remained independently listed; the effect of survivorship bias is addressed in Section 7.)

2. Why Early Multiples Were So High

When Apple went public in 1980, the global venture capital industry had a total footprint of less than $5 billion—a figure that had only begun to grow after the Department of Labor’s 1979 relaxation of the “Prudent Man Rule,” which allowed pension funds to invest in risk assets. Apple’s IPO was the largest U.S. technology offering since Ford Motor’s 1956 debut. The company had just 2,650 employees, was four years old, and its business model was far from well understood. Private capital lacked the capacity to sustain a company in private hands for long—companies needed public market capital to survive and expand, which meant they went public when they were still small.

Nvidia went public in 1999 at a market cap of just $230 million. Jensen Huang had founded the company in 1993 with $200,000 in seed capital, and had launched the world’s first GPU—the GeForce 256—only the year before the IPO. The potential of GPU computing was entirely unpriced; no one could have known that AI training would become the defining computational demand of the 2020s. Amazon listed in 1997 at $430 million; its cloud business wouldn’t exist for another nine years. Public market investors effectively played the role of venture capitalists: entering at minimal valuations, bearing early-stage uncertainty, and earning the potential for hundred- or even thousand-fold returns in exchange.

3. The Inflection Point: Meta (2012)

In retrospect, Meta’s IPO represents a structural dividing line. In 2012, Facebook listed at a $104 billion valuation—the largest U.S. technology IPO in history at the time. Before this, no technology company had been able to sustain itself in private hands at anything close to that scale.

Sequoia, DST Global, Goldman Sachs, and others had steadily added to their Facebook private-market positions, driving the valuation from $23 billion in 2010 to $104 billion at IPO. Notably, between 2010 and 2011, SharesPost and SecondMarket—two private secondary platforms—emerged specifically to provide liquidity for Facebook employees and early investors. It was the first time in history that such a systematic mechanism existed to let insiders exit without a public offering. Then, in April 2012, President Obama signed the JOBS Act, raising the mandatory SEC registration threshold from 500 to 2,000 shareholders—directly extending the legal window for high-quality companies to remain private. Facebook’s IPO arrived in this context: by the time ordinary investors could buy in, the company’s most explosive early-growth phase was already behind it. Meta has appreciated roughly 16x from its IPO to today—not a bad result for a hundred-billion-dollar company; a 16x return is outstanding by any asset-class standard.

Meta’s significance lies not in the fact that “16x wasn’t high enough,” but in what it demonstrated for the first time: a hundred-billion-dollar technology company could complete the majority of its value discovery before going public. The 100x or 1,000x early-growth phase that had historically been the preserve of public market investors had already been absorbed by private capital before Facebook ever opened to the public. This was the first clear signal that Public Market Alpha was beginning to migrate systematically into Private Market Alpha.

From Meta onward, the playbook was set: raise private rounds, delay the IPO, go public at a significantly higher valuation.

4. Today’s Three Prospectuses

SpaceX (combined with xAI) publicly filed its S-1 on May 20, targeting a $1.75 trillion valuation, with a pricing window as early as June 11. This is no longer simply a rocket company: following the xAI merger, the entity now integrates orbital launch, Starlink satellite internet, the Grok AI platform, and the Colossus data center—home to more than 220,000 Nvidia GPUs—under a single corporate umbrella.

OpenAI filed its S-1 confidentially on May 22, targeting a September listing at a post-money valuation of approximately $852 billion. The company recorded $13.1 billion in revenue in 2025, but spent approximately $22 billion, and is projected to lose $14 billion in 2026. CFO Sara Friar has privately acknowledged that the company is “not yet ready” to be a public company.

Anthropic has retained Wilson Sonsini to begin legal preparations, targeting an October IPO at a current private valuation of approximately $900 billion, with a target raise exceeding $60 billion. Amazon and Alphabet are both major shareholders; Broadcom has signed an agreement to supply 3.5 gigawatts of TPU compute capacity beginning in 2027. Anthropic generated annualized revenue of roughly $3–4 billion in 2025, but continues to run significant losses.

None of these three companies has yet listed, yet their current valuations are already thousands of times the market capitalization at which Nvidia debuted in 1999. In other words, the phase that historically left the most upside for public market investors—the early stage of maximum uncertainty and minimal valuation—is increasingly being absorbed by private capital before the IPO ever happens. The public offering is shifting from an entry point for ordinary investors into early-stage innovation, to an exit ramp for private capital to monetize maturing assets.

5. Why This Is Happening: Three Mutually Reinforcing Structures

Private capital supply has expanded dramatically.

Global private market AUM has grown from roughly $3 trillion in 2010 to more than $15 trillion by 2025—a more than fivefold increase. The influx of SoftBank Vision Fund, sovereign wealth funds, and crossover funds such as Tiger Global and Coatue means that high-quality companies can raise more than sufficient capital in the private markets without ever needing to go public.

Public company compliance costs have risen sharply.

Since the Sarbanes-Oxley Act of 2002, the financial and internal-controls compliance burden on public companies has increased substantially. The marginal cost of going public early now meaningfully exceeds the cost of remaining private, creating a strong incentive to delay.

Founder preference for control has strengthened.

This generation of founders has both the will and the means to maintain long-term control through private financing. Dual-class share structures further reduce the opportunity cost of delaying a listing.

Of the three, the expansion of private capital supply is the primary driver—without it, the other two factors would have limited effect. Rising compliance costs and founder control preferences are accelerating forces, not root causes. Together, the three reinforce one another, continuously pushing IPO timing later and IPO valuations higher.

6. Two Types of Companies, Two Different Logics

There is an important distinction within this framework: not all companies are “pre-priced” in the same way. Separating two types of companies is practically useful when assessing the post-IPO growth runway.

Type 1: Infrastructure companies.

Nvidia, Amazon, SpaceX, OpenAI, Anthropic. The defining characteristic of this category is that these companies can still enter entirely new technology platform cycles after listing. Nvidia went public as a GPU gaming card company; the AI training wave came 20 years later. Amazon was a bookseller; AWS didn’t exist until nine years after the IPO. Each new platform cycle resets the ceiling on their growth runway, weakening the constraint that the IPO valuation places on future returns. This explains what looks like a paradox: Google listed at $23 billion in 2004—looking “expensive” at the time—but subsequently entered multiple new cycles: search advertising at scale, Android, YouTube, cloud, and AI. It went on to appreciate approximately 200-fold. The IPO did not price these platforms; they were discovered afterward.

Type 2: Platform application companies.

Meta, Uber, CrowdStrike. These companies list with a relatively legible business model; their growth logic depends more on scaling, margin expansion, and market share consolidation than on the opening of an entirely new platform. Investors pay a “certainty premium,” not a “future platform option.” Subsequent upside is therefore more directly constrained by the IPO valuation.

The three incoming AI companies sit at the intersection of both logics. Model capabilities and physical compute infrastructure carry the hallmarks of infrastructure-type companies, and in theory they could enter new platform cycles. But the starting valuations—$1.75 trillion for SpaceX, $852 billion for OpenAI, $900 billion for Anthropic—imply that these platform options are already substantially priced in. What remains for public market investors is a bet on whether those platform options will deliver beyond expectations—not a bet on whether those options exist at all.

7. The Limits of the Data: Survivorship Bias

This framework has a limitation that deserves honest acknowledgment: every company in the analysis is a survivor. Apple, Nvidia, and Amazon all made it; the vast majority of companies that went public at equally small valuations during the same periods went to zero and are nowhere to be seen.

Two counterexamples help calibrate intuition. Webvan went public in 1999 at a market cap of roughly $4.8 billion, billed as the pioneering online grocery company of its era—low valuation, early listing. It filed for bankruptcy in July 2001 after burning through more than $1.2 billion in cash, leaving shareholders with nothing. Groupon listed in 2011 at roughly $12.7 billion and was once described as the fastest-growing internet company in history; at IPO it appeared to be a relatively undervalued early-stage bet. Today it trades at less than $500 million—more than 96% below its IPO price. Both companies went public at valuations far lower than Meta’s, yet public market investors suffered complete losses, not multiples.

The conclusion “early IPO = high growth multiple” requires a precondition: the ability to identify genuinely high-quality companies. Without that, a low early valuation does not translate into actual returns. Conversely, “late IPO = limited upside” is not absolute. If a company enters a new, still-unpriced growth phase after listing, secondary market investors can still earn strong returns. Among top-tier technology companies, however, that scenario is becoming increasingly rare.

8. Conclusion

Private markets are partially opening to the public. Platforms such as Forge Global and EquityZen offer private secondary market liquidity; major asset managers are launching private fund products for high-net-worth individuals. This window is widening, but meaningful barriers remain.

There are still “small and undervalued” companies in the public markets. The search for the next high-quality company entering the public arena at an early stage remains logically sound—it has simply become harder, not impossible.

The role of the public market is undergoing a structural transformation: it is shifting from “discovering the future” to “providing liquidity for a future that has already been partially discovered by private capital.” Technology IPOs are increasingly less an entry point for ordinary investors into early-stage innovation, and more an exit ramp for private capital to monetize mature assets. This is not a pessimistic verdict—it is an accurate description of a role change that has already taken place. The secondary market still offers opportunities, but the job description has changed: no longer bearing early-stage startup risk at minimal valuations in exchange for hundred-fold returns, but participating at reasonable prices in the continued appreciation of already-validated growth assets. Understanding this distinction is the first step to recalibrating a public market investment framework.