Why the Anthropic and OpenAI Revenue Figures You’re Seeing Are Not Measured on the Same Basis

Introduction: Two Numbers, One Misreading

In April 2026, the technology press erupted in near-unison: Anthropic’s annualized run rate (ARR) had broken through $30 billion, surpassing OpenAI’s $25 billion. Headlines declaring an “AI landscape reversal” blanketed the news cycle for several days.

Yet the vast majority of coverage quietly skipped over a fundamental issue when drawing this comparison:

These two numbers were measured with entirely different rulers — not because of different accounting choices, but because the legal relationships each company has with its core partner are structurally different from the outset.

This article explains where that structural difference comes from, why it determines the revenue basis, and whether the April 27, 2026 restructured agreement is beginning to close the gap.

Core Conclusions: Read This First

Before reading the rest of this article, here are the conclusions up front.

“Anthropic ARR $30B, surpassing OpenAI’s $25B” is a comparison made with two different rulers. Anthropic reports gross revenue; OpenAI (at least through its Microsoft cloud channel) reports net revenue. This is not a case of two companies actively choosing different accounting policies — it is a structural difference already embedded at the legal contract level in each company’s relationship with its core partner.

Three key conclusions:

Conclusion 1 Anthropic is the legal seller: on Amazon’s cloud marketplace, the seller field on enterprise customer invoices reads “Anthropic, PBC.” Amazon provides the infrastructure, but Anthropic bears the delivery obligation — and must therefore report gross revenue under accounting standards. The channel fee paid to Amazon is recognized as a cost after revenue recognition, not netted against total revenue.

Conclusion 2 OpenAI reports net revenue at least through the Microsoft cloud channel: enterprise customers contract and pay Microsoft directly; Microsoft is the legal seller, and OpenAI receives only the net settlement Microsoft remits. Furthermore, OpenAI’s contract with Microsoft requires it to remit 20% of all gross revenue to Microsoft, further compressing the revenue basis OpenAI can actually recognize.

Conclusion 3 The new agreement reshapes the landscape, but convergence takes time: the April 27, 2026 restructuring removed the exclusivity restriction, and OpenAI promptly launched on Amazon’s cloud platform. This creates the conditions for future convergence in revenue basis — but as long as the 20% revenue share obligation continues (contractually through 2030, up to a cumulative cap of $38 billion), the foundation of the discrepancy will not disappear.

With these three conclusions in mind, every supporting argument that follows will be clearer.

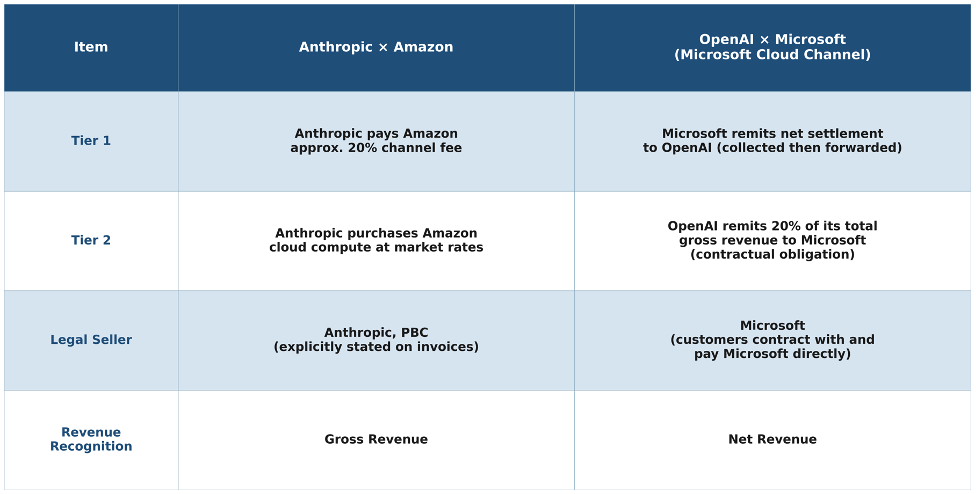

1 A Similar Two-Tier Structure — Symmetrical on the Surface, Different in Nature

The revenue-sharing arrangements between each company and its core platform partner both appear to involve two tiers of outflows, creating a superficially symmetrical picture. The table below presents them side by side:

The symmetry is only skin-deep. The two tiers differ fundamentally in nature, calculation basis, and the timing of revenue recognition — and it is precisely these differences that determine why the two companies must report revenue on different bases.

2 The Root of the Discrepancy: Who Is the Legal Seller

ASC 606, the US GAAP revenue recognition standard, asks just one question: when a customer pays for an AI service, who is the legal seller? If you are the “Principal” — controlling the service and bearing the delivery obligation — you report gross revenue. If you are the “Agent” — completing a transaction on behalf of another party — you report net revenue.

For Anthropic, the answer is straightforward. For OpenAI, it is considerably more complex.

Anthropic: The Invoice Says “Sold by Anthropic”

On Amazon’s cloud marketplace, the seller field on enterprise customer invoices reads “Anthropic, PBC.” This is not a marketing statement — it is a legal fact: Amazon provides the infrastructure, but Anthropic is the contractual delivery party. AWS official documentation states this explicitly, and it is corroborated by actual customer invoices.

Under this standard, the determination is direct and unambiguous: Anthropic is the principal and must report gross revenue. The channel fee paid to Amazon is recorded as an expense after revenue recognition and does not reduce total revenue.

More critically, Anthropic has no contractual requirement to allocate any percentage to a partner before revenue is recognized. Every dollar from every channel flows into Anthropic’s total revenue first, before costs are deducted.

OpenAI: Two Channels, Two Mechanisms, Both Pointing to Net Revenue

OpenAI has always operated two parallel API channels simultaneously. Understanding this is a prerequisite for understanding the revenue basis question — because the following two mechanisms each independently push both channels toward net revenue recognition.

Microsoft Cloud Channel (Net Revenue — Structurally Certain)

Enterprise customers contract and pay Microsoft directly; Microsoft is the invoiced seller. OpenAI receives only Microsoft’s net settlement and never sees the gross amount. Under this standard, OpenAI is an agent on this channel and must report net revenue. There is no ambiguity here — it is not an accounting policy choice but the inevitable conclusion of the contractual structure.

Direct API Channel (Net Revenue — Most Likely; Pending S-1 Confirmation)

platform.openai.com is operated by OpenAI itself, making OpenAI the invoiced seller. However, a critical constraint applies: OpenAI’s contract with Microsoft requires OpenAI to remit 20% of its total gross revenue to Microsoft — across all channels, covering both the Microsoft cloud channel and direct API. TechCrunch reported in May 2025, citing leaked documents:

“OpenAI currently has an agreement to share 20% of its top line with Microsoft.” — TechCrunch, May 2025 (verified via leaked documents)

This is the direct connection between the two channels and the revenue basis question: the 20% obligation’s scope extends beyond the Microsoft cloud channel — it applies equally to the direct API channel. If this 20% is contractually deducted before revenue attribution, then OpenAI can only recognize $0.80 on the dollar on the direct API channel, making the basis net revenue. If it is recorded as an expense after revenue recognition, the direct API channel remains gross revenue. This accounting treatment detail has not been confirmed in any audited public disclosure and must await the S-1 filing.

In summary: net revenue on the Microsoft cloud channel is structurally certain; net revenue on the direct API channel is highly probable but strictly speaking unconfirmed. Both point in the same direction.

The Revenue Basis Is Not a Deliberate Choice — It Is the Inevitable Result of Legal Structure

In an internal memo dated April 13, 2026, OpenAI’s Chief Revenue Officer Denise Dresser criticized Anthropic for using a gross revenue basis, calling OpenAI’s net revenue basis “more consistent with public company standards.” This criticism has a fundamental flaw: Anthropic reports gross revenue because its Amazon cloud contract structure makes it the legal seller — it has no choice. OpenAI reports net revenue on the Microsoft cloud channel because Microsoft is the legal seller — equally, it has no choice. Both are faithfully reflecting their respective legal realities, not exercising accounting options.

The deeper irony: approximately two weeks after the memo was sent, OpenAI itself went live on Amazon’s cloud platform. If OpenAI is the seller entity on this new channel (analogous to Anthropic’s structure on the Amazon marketplace), that portion of revenue would be reported on a gross basis — creating a situation where OpenAI internally operates under two different revenue bases simultaneously, which would need to be reconciled in the IPO filing.

3 How Large Is the Gap, and Can It Be Converted?

The confirmed portion of the revenue basis discrepancy stems from one structural fact: Anthropic is the invoiced seller on Amazon’s cloud marketplace and reports gross revenue; on OpenAI’s Microsoft cloud channel, Microsoft is the invoiced seller and OpenAI reports net revenue. This portion of the difference is certain.

What cannot yet be confirmed: OpenAI’s 20% obligation covers its direct API channel, but whether that revenue share is deducted before or after revenue recognition has not been confirmed in any publicly audited disclosure. Therefore, a precise apples-to-apples conversion of the two figures has no reliable basis before S-1 filings are made.

The direct comparison of “$30B vs. $25B” is incomplete — the two numbers have a structural difference in basis, but the precise magnitude of that difference cannot be determined until S-1 filings are submitted.

4 What the New Agreement (April 27, 2026) Changes

The April 27 Microsoft–OpenAI agreement amendment, and the simultaneous launch on Amazon’s cloud platform (April 28), fundamentally altered OpenAI’s distribution landscape. Key changes in the agreement:

① Microsoft cloud exclusivity terminated; Microsoft IP license converted to non-exclusive (through 2032): OpenAI may offer its full product suite on any cloud platform. Microsoft’s license to use OpenAI’s IP models was changed from exclusive to non-exclusive, with an extended effective date through 2032.

② 20% revenue share maintained through 2030, with a new cumulative cap of $38 billion (The Information, May 12, 2026; corroborated by Reuters).

③ Microsoft ceases paying OpenAI channel rebate shares: the flow of revenue sharing became unidirectional — OpenAI pays Microsoft only.

④ OpenAI models officially launched on Amazon’s cloud platform: Amazon’s cloud service became the exclusive third-party cloud distributor for OpenAI Frontier enterprise platform.

4.1 Is OpenAI the Seller on the Amazon Cloud Channel? — That Is the Critical Question

platform.openai.com has always been OpenAI’s own direct API, making OpenAI the seller. The Amazon cloud channel raises a new question: if OpenAI is also the seller entity on this new channel (analogous to Anthropic’s structure on Amazon’s marketplace), and Amazon does not impose a similar 20% revenue share arrangement, then revenue from this channel would be reported on a gross basis — fully consistent with Anthropic.

This would create a genuine dual-basis situation within OpenAI: channels subject to the 20% revenue share obligation (all existing revenue) reported on a net basis, and the new channel not subject to that obligation (Amazon cloud) reported on a gross basis. Such a dual-basis situation cannot be maintained in an IPO filing — the SEC will inevitably require uniformity.

4.2 Will the Two Companies Converge?

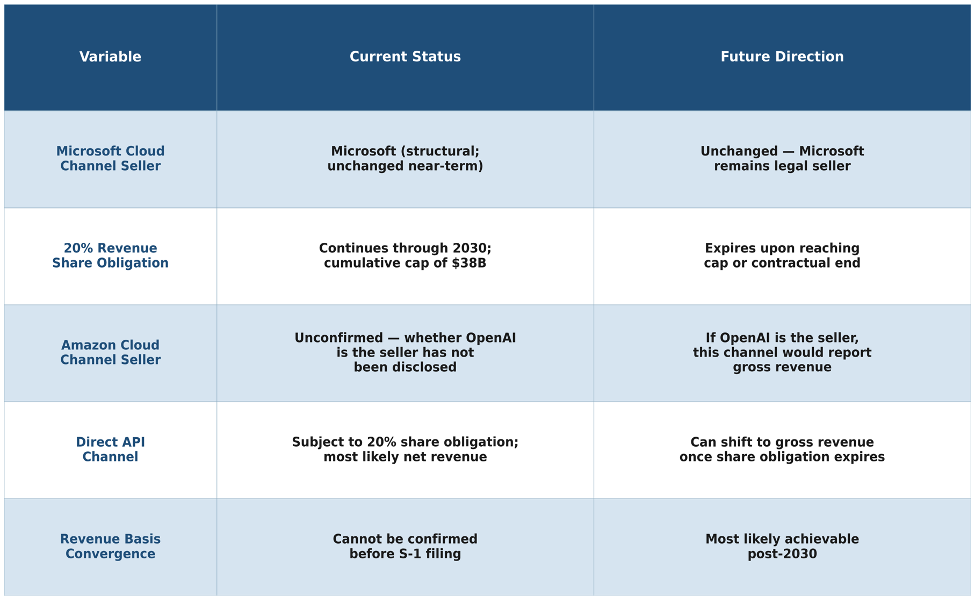

From a structural logic standpoint, the direction of convergence is almost certain. The table below analyzes each key variable:

The most critical long-term variable is when the 20% revenue share obligation cumulatively reaches its cap ($38 billion, with 2030 as the final deadline), and whether the Amazon cloud channel is subject to a similar revenue share arrangement. The fundamental reason for Microsoft cloud channel net revenue reporting is Microsoft’s seller status — that structure will not change when the obligation expires. But the basis for OpenAI’s other channels could theoretically shift toward gross revenue once the obligation disappears.

5 IPO Perspective: Standardizing Revenue Basis Is a Test Both Companies Face

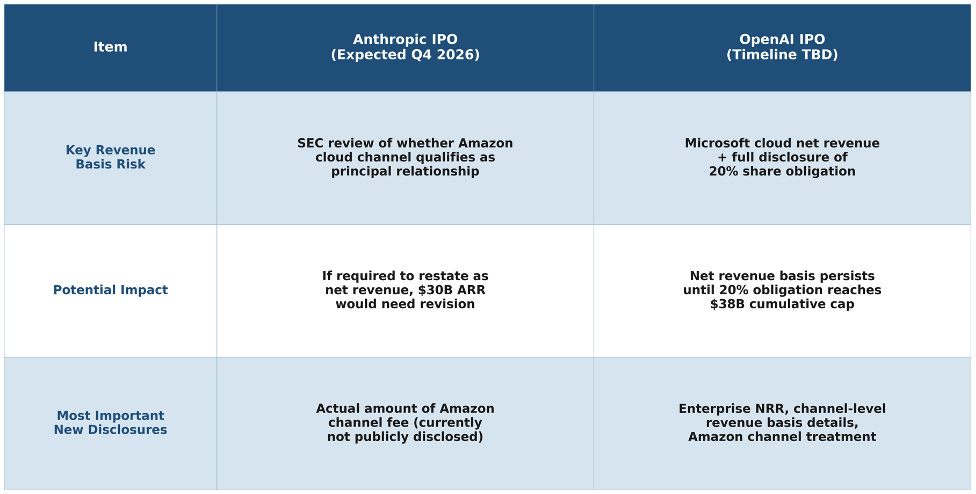

5.1 Anthropic: Can the Gross Revenue Basis Hold?

Anthropic is expected to file its S-1 as early as Q4 2026. The ASC 606 determination of principal status will determine whether it can maintain a gross revenue basis:

If the SEC requires a shift to net revenue reporting, Anthropic’s $30 billion figure would need to be restated net of channel fees, altering the slope of its historical growth curve and affecting valuation modeling. The magnitude of the adjustment depends on the actual channel fee amount, for which no audited figures are currently available. This single item alone could be the most important financial variable heading into the IPO.

5.2 OpenAI: Greater Disclosure Pressure and More Complex Revenue Basis Issues

Once in the SEC review process, the following three items will almost inevitably require full disclosure:

● Enterprise NRR must be disclosed: The enterprise net revenue retention rate (NRR — the ratio of the following year’s actual renewal revenue from existing customers to the prior year’s revenue) has never been publicly disclosed. It is the most critical valuation metric for subscription software companies, and the SEC will require it.

● Full details of the Microsoft agreement must be disclosed: The 20% revenue share percentage has been publicly confirmed, and the cumulative cap ($38 billion) has been reported by The Information, but the scope of the share across individual channels and the specific trigger conditions still need to be fully described in IPO filings.

● Revenue basis for the Amazon cloud channel must be determined: Does the 20% revenue share obligation cover revenue from this channel? If not, this revenue should be reported gross, at which point the company would have two concurrent revenue bases — and the IPO filing would need to address this explicitly.

5.3 Special Risks of Both Companies Going Public in Close Proximity

If both companies list within a narrow window in late 2026, they will collectively draw down the first wave of capital allocation directed at pure-play AI equities. Once the SEC mandates a uniform revenue basis, investors will for the first time see truly comparable numbers for both companies — the gap that emerges may be narrower than the current narrative suggests, or it may be wider.

Conclusion: Understand the Structure Before Asking Who Is Ahead

“The AI industry is at a historic inflection point in the standardization of revenue recognition frameworks. Before S-1 filings are made, every ARR figure investors encounter should prompt two questions: on whose books is this revenue being recognized? And is there a revenue share obligation that precedes recognition?”