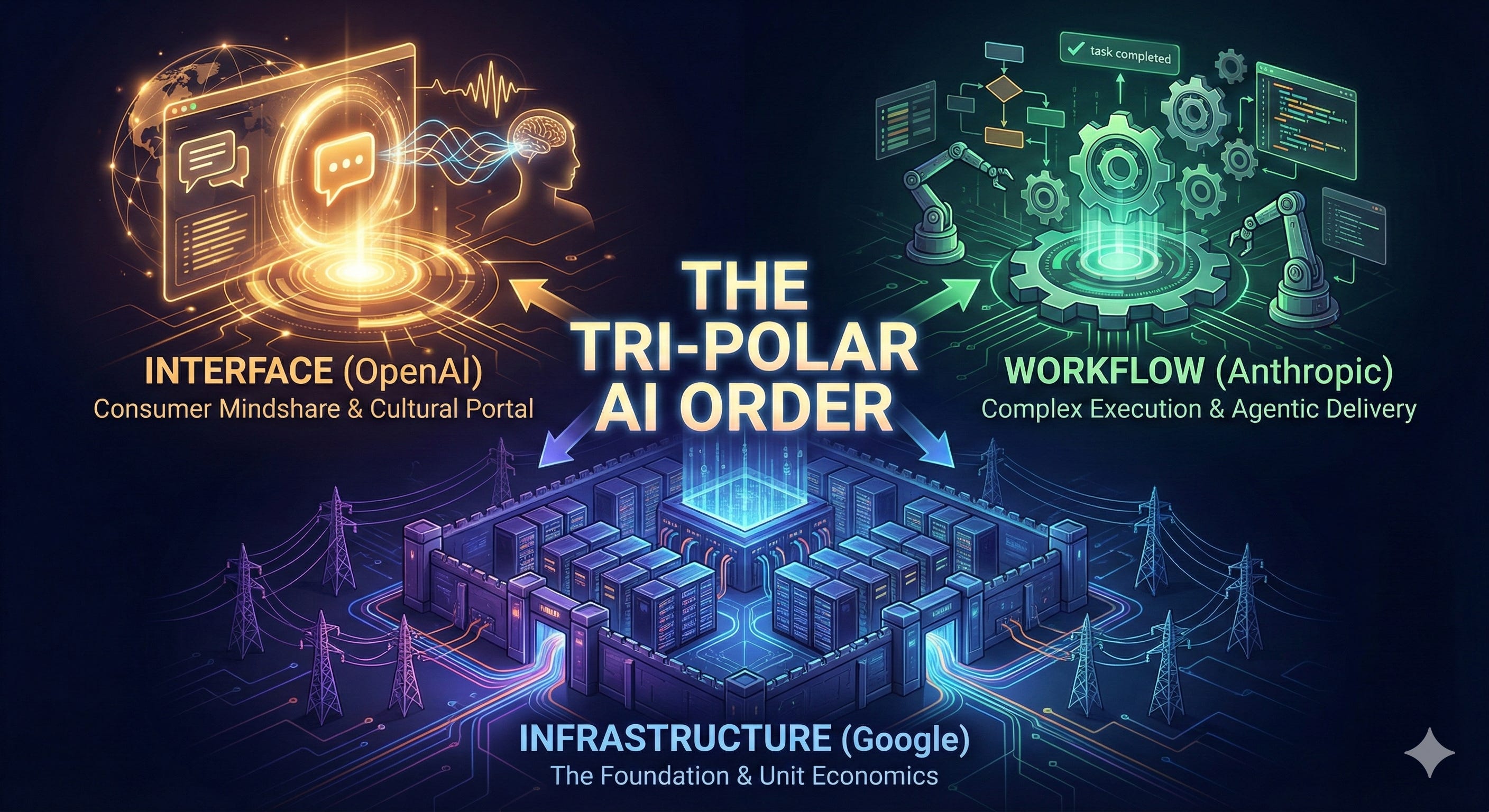

🛰️ The World After Benchmarks

By February 2026, with the release of Claude Opus 4.6, the AI industry has officially moved past the stage of “linear intelligence competition.” The industry no longer ranks models solely by ELO scores; instead, three distinct centers of gravity have formed based on Functional Ideology.

This market structure is now defined as the Tri-Polar Order:

Google (The Sovereign): Leads the physical layer and unit economics.

OpenAI (The Celebrity): Leads consumer mindshare and distribution networks.

Anthropic (The Assassin/Executor): Leads complex workflows and agentic delivery.

We argue that while these three titans currently occupy their own territories, this equilibrium is transient and fragile. Technical decision-makers must shift from asking “which model is strongest” to “which ecosystem best aligns with my operational requirements.”

🏗️ 1. Google: The Victory of Physical Unit Economics

Strategic Positioning: The Sovereign

Core Advantage: Full-Stack Vertical Integration

Google’s strategic focus has shifted from model parameters to infrastructural sovereignty. While Gemini may not lead in every creative task, Google is leveraging its physical layer advantages to build an impenetrable moat for enterprise deployment.

The Silicon Dividend: According to IDC’s 2025 Cloud Tracking data, the large-scale deployment of the TPU v6 Trillium clusters has allowed Google to drive marginal inference costs for long-context tasks 18%–22% lower than cloud providers relying on general-purpose GPUs. This allows Google to treat AI as a “utility” (similar to electricity), dominating cost-sensitive enterprise sectors.

Frictionless Distribution: For Global 2000 firms, Gemini is not a new tool to be “adopted” but a native feature to be “activated” within Google Workspace. The power of the Default Option ensures that Google maintains a high defensive barrier in the foundational enterprise productivity layer.

🎭 2. OpenAI: The Cultural Interface and Dual-Front Pressure

Strategic Positioning: The Celebrity

Core Advantage: Consumer Mindshare & Brand Interface

OpenAI remains the “Start Button” of the internet. SimilarWeb data indicates that ChatGPT and its derivative products (Sora, Voice) command 64% of global consumer AI traffic.

The Cultural Moat: OpenAI has successfully turned “GPT” into a synonym for “Search.” In multimodal creativity and real-time voice interaction, their user experience remains 6–9 months ahead of the pack. They are the primary touchpoint for the masses.

Structural Challenges: OpenAI faces a classic “dual-front war”:

Downstream: A lack of proprietary silicon subjects their inference cost structure to external parties (primarily Microsoft and NVIDIA).

Lateral: In the domain of complex logic and code generation, they are facing functional displacement by Anthropic.

🧠 3. Anthropic: The Paradigm Shift from “Chat” to “Execution”

Strategic Positioning: The Assassin (The Executor)

Core Advantage: Complex Task Success Rate

The release of Claude Opus 4.6 marks the transition of the AI value chain from “providing information” to “delivering results.”

Architectural Inference: Based on its performance in SWE-bench, Opus 4.6 likely integrates a Native OS Sandbox within its inference environment. It is no longer just generating code; it demonstrates a closed-loop “Write-Test-Fix” capability. This behavior suggests an architectural evolution from “Next-Token Prediction” toward Multi-step Planning and Reasoning.

Agentic Penetration: Within Fortune 500 engineering teams, Claude is rapidly becoming the preferred “pair programmer.” It is not just an assistant, but an autonomous junior engineer with independent execution rights.

🌋 4. Industry Impact: Structural Reform and Lag

The crystallization of the Tri-Polar Order will have profound structural impacts on downstream industries, forcing a total reconstruction of legacy business models.

IT Services: Structural Margin Compression (Infosys, Wipro, Cognizant): The traditional “FTE-based (Full-Time Equivalent) pricing” model is facing an existential crisis. As models like Opus 4.6 drive the marginal cost of junior-level code generation toward zero, clients will refuse to pay for simple human hours. While revenue displacement may not happen overnight, the erosion of pricing power will manifest in the next 24 months, forcing service providers to pivot from “labor arbitrage” to “result-based delivery.”

The Death of “Thin Wrappers”: SaaS companies that only provide a simple UI or preset prompts on top of foundational models are losing value rapidly. As base models natively integrate long-context and agentic workflow capabilities, the value space for middlemen is being crushed.

The Microsoft Paradox: The Utility Risk: Microsoft faces the strategic risk of becoming the “ISP of Productivity.” While they own the strongest distribution channels (Windows/Office), if the high-value cognitive reasoning migrates to Anthropic or Google via API, Microsoft may only earn the “connectivity fee” while losing the “intelligence premium” to others.

🧭 5. The Operator’s Playbook: How to Survive the Tri-Polar World

The crystallization of this Tri-Polar Order implies that the era of “Model Loyalty” is over. We are entering the era of “Model Routing.”

For Developers: Build the “Router,” Not the Wrapper: Stop debating whether GPT-5 or Claude Opus is “better.” Use Anthropic (The Assassin) for the “Critical Path”—complex logic loops and code generation. Use Google (The Sovereign) for the “Heavy Lifting”—processing massive context windows. Use OpenAI (The Celebrity) for the “Last Mile”—natural language formatting and user interaction.

For Founders: The “Service-as-Software” Pivot: The “Thin Wrapper” era is officially dead. With Anthropic’s dominance in agentic workflows, the opportunity is selling an agent that does the work. Move from SaaS (Software as a Service) to Service-as-Software.

For Enterprise Leaders: Beware the “Bundling Trap”: It is tempting to default to the Microsoft/OpenAI stack because it’s already in your Office 365 contract. While safe, this path risks leaving your organization with “Average Intelligence.” Do not let procurement convenience dictate your intelligence strategy.

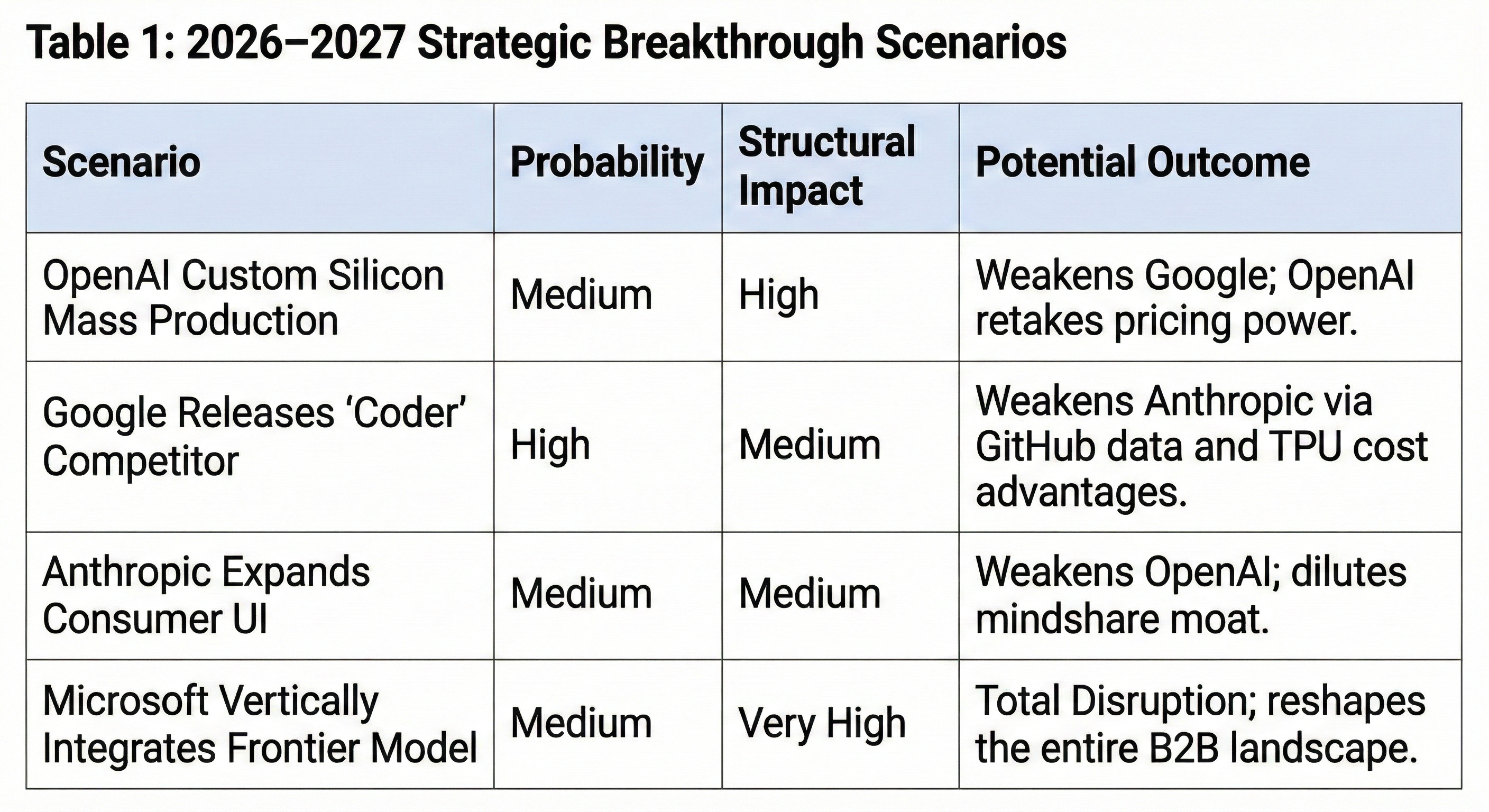

⚖️ 6. Strategic Outlook: The Stability Matrix

The current Tri-Polar Order is a transient equilibrium based on current silicon supply and model architectures. Functional Divergence is not Permanent Specialization; boundaries will inevitably blur as all three actors invest horizontally.

📖 Appendix: Technical Deconstruction & Empirical Anchors

This appendix provides technical specifications and market data to support the strategic deductions in the main text.

🧪 Claude Opus 4.6: Technical Analysis

The paradigm shift in Opus 4.6 is driven by three architectural innovations:

Native OS Sandbox: Unlike GPT-5, Opus 4.6 exhibits traits of a lightweight Linux kernel integrated directly into the inference environment. This gives the model “proprioception”—it can compile, run, and debug in a local environment.

Intrinsic Multi-Agent Orchestration: When handling complex tasks, Opus 4.6 automatically “forks” into multiple sub-agents communicating internally. This mechanism significantly reduces hallucination rates.

Active Inference Loop: The model actively seeks actions that minimize uncertainty before finalizing an output, moving away from pure next-token prediction.

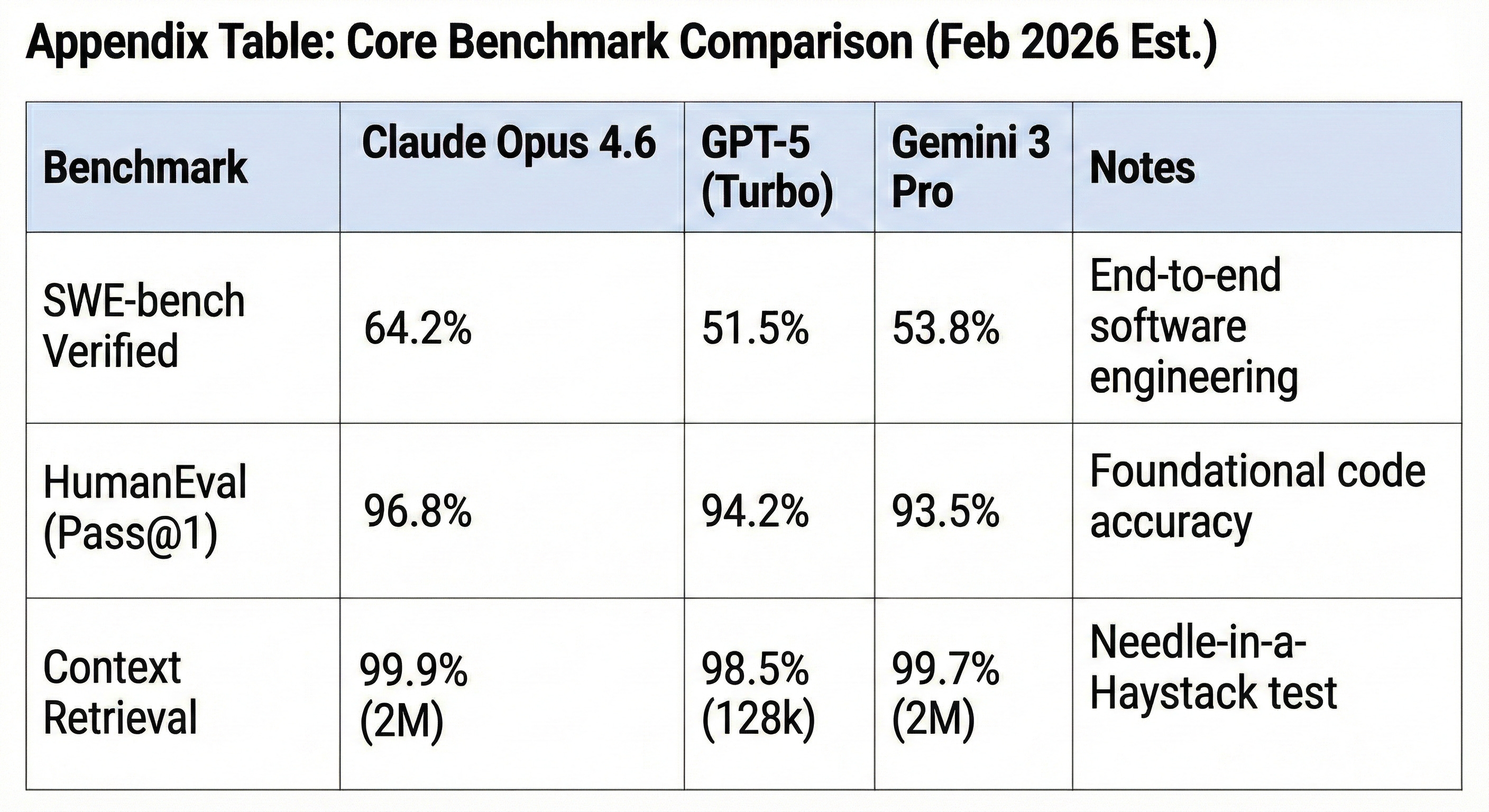

📊 Core Benchmark Comparison (Feb 2026 Est.)

Note: Figures represent weighted averages of publicly available benchmark runs as of February 2026.

📉 Market Telemetry: Why Now?

Enterprise Coding Adoption: According to the Menlo Ventures 2025 State of AI Report, Anthropic’s API invocation within Fortune 500 IDPs grew by 410% in the last six months.

The “Why Now” Factor: The February 2026 timing is the intersection of the “Moore’s Law Lag” and “Application Layer Awakening.” After 18 months of “PoC Purgatory,” enterprises realized simple chatbots couldn’t solve core business logic.